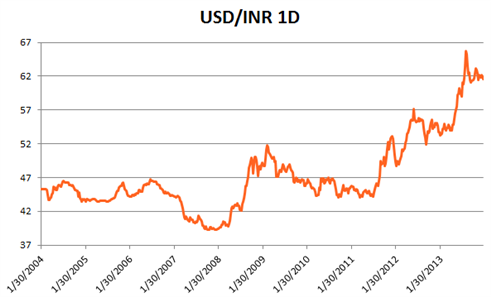

From its August 2013 (and all time) lows, the Indian Rupee (INR) has recovered about 10% of its value against the Dollar. Looking at the Rupee on a longer term time scale, however, puts that recent move into perspective (see USD/INR 1D). The Indian economy has hardly been stellar relative to the rest of emerging markets over the past five years and this, among other factors detailed in this report, have plagued the Rupee over the past decade.

Although India shares similar, growth encouraging factors such as China- mainly a large workforce able to be employed at relatively low wages in the manufacturing and production sectors- India still falls behind in most measurements, including GDP growth. India ranks 38 countries below China in the World Bank’s Ease of Doing Business Index the nation is plagued by weak and disorganized infrastructure, power outages, corruption and a ramped beaurocracy. So when little to no growth in the West after the financial crisis forced investors to scour the globe for higher and more stable returns, India didn’t benefit. Those nations who exported raw materials to China, on the other hand, saw their economies grow and currencies strengthen.

But notably, as will become increasingly more relevant as debt markets tighten in 2014, India never had the exorbitant credit expansion and state led investments that have been the engine of Chinese growth over the past five years. That may benefit them in coming out of any EM hard-landing. The stimulus from Beijing in 2009 propelled commodity bloc currencies higher as China devoured their raw materials. With under 5% of India’s exports being consumed by China on an annual basis, the Indian economy did not ride the Chinese stimulus wave and instead was hampered by weaker growth in the West. In the five years since the financial crisis, the Rupee is trading a full 57% lower against the greenback.

Narrowing in on price action over the past year, the rapid depreciation of the Rupee in 2013 can be attributed to a number of external and internal factors. As we detailed in August, the Federal Reserve’s rhetoric in late May hinting at an upcoming reduction in asset purchases fueled a massive correction to the downside- not only in the Rupee, but also in those currencies whose appreciation was fueled by carry positioning and commodity bloc strength (ZAR, BRL, MXN, AUD, NZD). However over the last few months the Rupee is trading 10% higher against the greenback and the USD/INR pair has since remained trading in a relatively tight and stable range.

An internal factor that has impacted the Rupee has been a massive trade balance deficit and a declining level of foreign direct investment (FDI). India has been hampered by higher ICE Brent crude prices since the 2008 spike and those extra expenditures have drained growth potential. In addition, India is a large consumer of gold and the appreciation of the commodity over the past five years has increased India’s imports in value weighed terms. Gold’s demand has been on the rise too as citizens have bought the commodity as a store of value in the face of higher inflation levels. This pushed the government to enact import curbing measures in 2013, and the import value of gold in India has since retreated from May highs. According to sources within the Indian government, the measures are said to remain in place until at least March.

The Rupee in 2014

United States

Excluding India’s expatriate workforce weighting, the United States is the largest contributor nation to India’s exports in terms trade value. From data starting in April 2012 and ending in September 2013, the U.S. accounted for almost 14% of India’s exports. Since the financial crisis it has often seemed to be the case that only credit expansion (ex. China) or export market growth (ex. Germany) have been able to propel GDP forward. In this zero-sum environment, a healthy return to growth and investment in the United States will have a substantial impact on India’s export market and thus her overall economy.

Inflation

For the Rupee to gain serious traction, holding the currency will have to show a real yield. With current benchmark interest rates out of the RBI far below inflation levels, there is an inherent risk in investing in the Indian economy. Until the spread narrows between the two, the Rupee is likely to remain under pressure. A pickup in exports vis-à-vis growth in the U.S. could free up the RBI to raise rates at a faster pace (see our Special Report on the RBI).

Emerging Market Risk

As the Federal Reserve winds down its asset purchase program over 2014, areas that have been most reliant on credit led growth are likely to be adversely impacted. As we learned in 2008, a tightening of credit conditions in an overleveraged system with improper risk controls and lax reporting standards will lead to disaster. Although we have seen a pullback in FDI and the currency strength of emerging markets since June, countries with capital controls and a heavy hand in the economy such as China have managed to hold on for now and contain risk.

Nevertheless, the fact that the People Republic Bank of China (PBOC) must pump tens of billions of Dollars on a moment’s notice into the inter-bank lending market (as was the case in January) is indicative of the overextended credit markets of China. A flight from risky assets in emerging markets would likely have less of an impact on India relative to other economies who rode the Chinese credit fueled expansion post-crisis. As credit conditions tighten on the back of a reduction in the Fed’s asset purchase program, investors may begin to seek safer yield over higher yields and this would benefit the West and by extent the Indian export economy. A slowdown in emerging markets and China could actually have a positive impact in the short run for India as lower energy prices could help cap troublesome inflation levels.

Written by Gregory Marks for DailyFX.com

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx