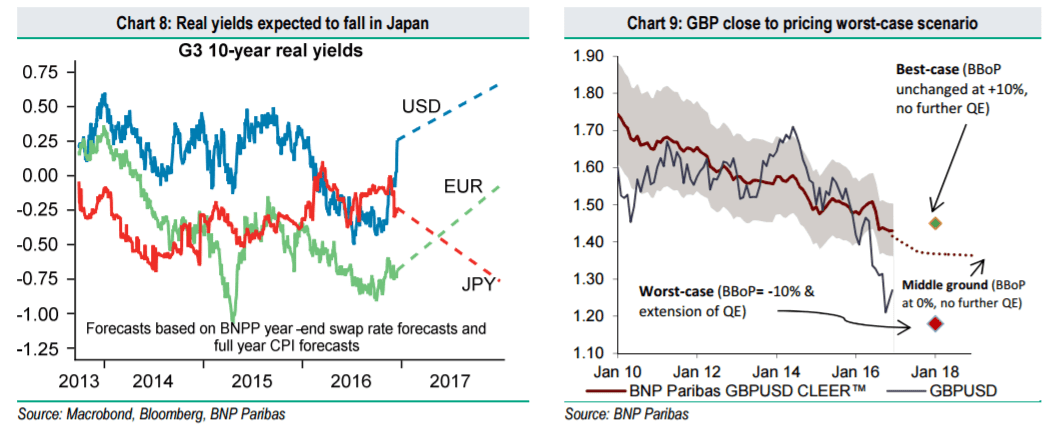

PY, the underperformer.

We view the yen as likely to be the weakest major currency in the G10 in 2017, with USDJPY reaching 128. Moreover, in contrast to our forecasts for other major currencies, we do not expect the yen to recover vs. the USD in 2018; instead, we forecast continuing depreciation.

We view the Bank of Japan’s yield curve targeting strategy as leaving the JPY particularly vulnerable in an environment of rising global reflationary pressures. While yield curves in most G10 economies will respond to rising inflation by steepening, the BoJ has signalled that it will aim to keep the 10yr JGB yield anchored around zero. Against this backdrop, rising global inflation expectations will act to depress Japanese real yields relative to real yields elsewhere, undermining the yen. At some level of yen weakness, our economists note that the BOJ could adjust higher its target for long-end yields, which would likely be an important, limiting factor on the extent to which the JPY could weaken.

GBP, the outperformer.

We expect the GBP to outperform most other G10 currencies in 2017, holding steady relative to a broadly firmer USD. The UK economy faces significant challenges in 2017 as it adjusts to Brexit uncertainty. However, as we have discussed in past Strategy publications, we think current levels of the GBP already price in a “worst-case” scenario for UK capital flows.

Moreover, there has already been a marked shift in UK government Brexit rhetoric, focusing less on immigration controls, and more on pro-business measures and the best possible single market access. GBP is trading very cheaply vs its long-term fair value and data suggest EM reserve managers are now comfortably, passively increasing GBP holdings.

Copyright © 2016 BNP Paribas™, eFXnews™Original Article