On Monday we have the first of three Trump- Clinton debates. Rare is the cut and thrust of these Presidential debates decisive. Kennedy-Nixon moments are few and far between. The ‘winner’ of the coming debates may well be the candidate that can break the mold of ‘confirmation bias’ and reveal something positive and new about themselves for swing voters. One immediately relevant question is: How should markets trade the post debate poll fluctuations?

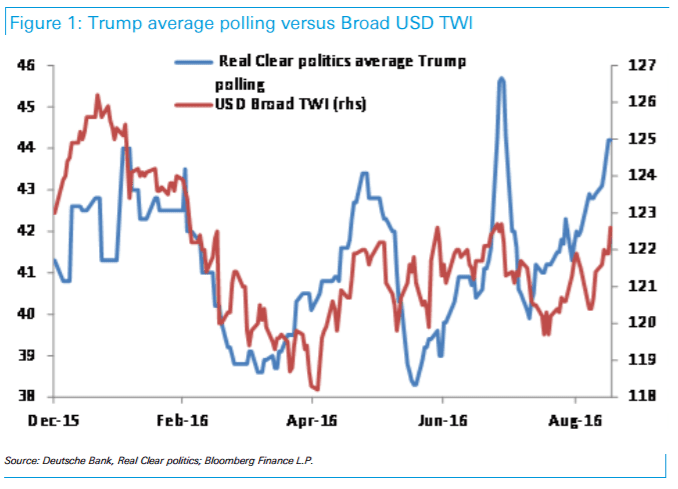

It has not felt like the market has traded the polls, but (very) superficially there has been a slight tendency for the USD to trade stronger when Trump has gone up in the poll (see Figure1). The average Real Clear Politics Trump poll correlation with the Broad USD TWI is 0.51 year to date, but almost certainly much of this correlation is spurious, especially in H1 when outside of USD/MXN, there was minimal anecdotal talk of trading off the polls.

Perhaps a more pertinent question is if you knew the election result today would you buy or sell the USD?

In so much as the current market talk has focused on the potential for a large fiscal stimulus whoever is the President and that this stimulus will encourage and complement monetary policy tightening, whoever is elected President is seen as a likely to be USD positive. Fears over a fiscal package that is too big or destabilizing are not high on the list, as there appears to be some belief in Congressional checks and balances. There is also some confidence that the election will break Washington’s gridlock long enough to get some stimulus through in the new President’s first year in office. The market is apt to trade off this one important strongly held belief, until it is confident that there are other policy initiatives to trade off. As an example, a USD negative allied to the election could relate to the attacks on free trade, where retaliation could easily constrain the Fed from tightening. The cult of personality will also be a factor. Who will be the next Treasury Secretary and will they use a weaker USD as a vehicle to support trade, as Lloyd Bentsen did in 1993 – 94? Nonetheless second order considerations like the above with all their uncertainties, are for the moment being dominated by positive USD fiscal arguments.

The big macro events to end 2016 may not all play out as decisively as hoped, but the skew as it relates to risks, all lean USD positive, whether it be probability for a Fed rate hike; the concerns around the Italian referendum; and soon to be most important, the prospective US election impact.

Copyright © 2016 DB, eFXnews™Original Article