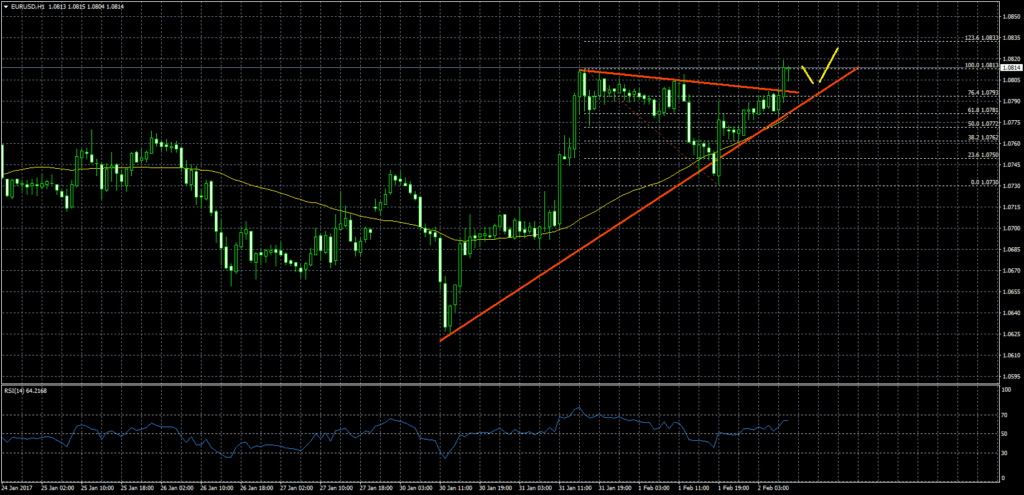

Goldman Sachs: No Changes; Cautious Tone But Slightly Hawkish.

BOE to close out week of central bank inaction. We also expect no changes to the current monetary policy stance in the UK, but we think the tone of the Press Conference, Inflation Report and MPC minutes will be quite cautious but tilt slightly hawkish

Morgan Stanley: GBP To 1.27/1.28 Before Lower.

This week the market focus will be on the BoE's inflation report. The market is still short GBP, suggesting that there is room for positioning adjustment to lift the currency. We think there is potential for GBP/USD to rally back to at least 1.27/1.28 before moving lower again towards our quarter-end target of 1.17

BofA Merrill: Chance Of Hawkish Feel; No Meaningful Impact On GBP

If the Bank of England (BoE) set interest rates on today’s growth and inflation they would likely hike rates on Thursday. But rate setters look forward to set policy. Given the weak sterling they are still balancing a likely inflation overshoot against likely growth weakness. So we expect a neutral bias on policy from the BoE, and expect them to hold rates and not extend QE this week. We think the risks are skewed to a hawkish message. Carney will likely emphasize that there are limits to the BoE’s inflation tolerance and conclude with a simple data watching position: steady as she goes for six months, but if growth does not slow then rate hikes will become more likely. Expectations going into next week's BoE meeting seem to have become increasingly polarized. While few on the Street seem to be forecasting an extension of QE at Thursday's meeting, market pricing in rates and our own sentiment surveys suggest investors remain split on QE. Consequently, we expect a hawkish reaction from the market to our central scenario of an end to QE and a relatively neutral BoE…Our economists' baseline scenario is unlikely to have a meaningful impact on GBP as this is pretty much the consensus view for the meeting

ANZ: Too Early To Call A Sustainable Turn In GBP.

Sterling has stabilised in recent weeks in part supported by speculation of a bi-lateral trade agreement with the US…However, outside of the potential for ‘squeezes’ in the market, the backdrop to the pound remains highly uncertain. PM May will trigger Article 50 before the end of March and the tone of the negotiations will be important in assessing sterling’s near term path. Meanwhile, whilst growth has impressed (Q4 GDP rose 0.6% q/q) and monetary policy is very supportive, there is a reasonable prospect that growth may slow from here. Hiring trends in the economy have slowed, real income growth will be eroded by rising inflation and investment may suffer. Whilst sterling has discounted a lot, it is still too early to call a sustainable turn.

NAB: BoE On Hold; GBP To Face FormidableResistance At 1.2775.

The key question is the extent to which this good political news is now already in the price of the pound? The sharp rally in GBP/USD reflects some disappointment with the USD as much as a less bleak near-term outlook for the GBP and, with the better growth and monetary policy outlook in the United States, we expect the USD to now gradually begin to find more investor support. The December 2016 high of GBP/USD1.2775 should provide formidable technical resistance to the recent rally and though the Bank of England on Thursday may try to talk tougher on inflation, no-one seriously expects a rate hike at any point over the next 12 months.

Barclays: BoE On Hold But Raises GDP Forecasts.

On Thursday, we expect the BoE to maintain its current policy parameters but likely higher GDP growth forecasts should support rate hike expectations and GBP. Given the strong performance of the UK economy over Q4, the Bank is likely to adjust higher its growth forecasts but may also note some concern about the sustainability of consumption, given the high level of household debt. The inflation forecasts are likely to stay unchanged as Q4 inflation was close to the bank’s forecast while a lessening of imported price pressures and higher UK interest rates are counterbalanced by higher inflation globally.

BTMU: BoE On Hold; Further GBP Upside.

While we do not expect a rate hike this year, we do expect the yield curve to adjust upwards as BoE rhetoric points to a greater desire to tighten monetary policy in 2018…Nonetheless, the resilience of the economy has been impressive and we see clear risks that the UK rates market will start to question the BoE easing from last August and speculation on a change in monetary stance is set to build later this year… We maintain our view of pound appreciation and are increasingly confident that the low-point for the pound post-Brexit is already behind us.

Credit Agricole: BoE On Hold, GBP Rallies A Sell.

The focus will be the BoE’s monetary policy announcement and inflation report. Essentially, we expect the MPC to reiterate its neutral policy outlook and not to renew its QE programme. As such, we expect limited currency impact. From a broader perspective, we believe GBP rallies should still be sold. The longterm outlook remains clouded by political uncertainty, while it cannot be excluded that incoming data will start to weaken more meaningfully. If so, medium-term inflation expectations might fail to break higher, leaving the BoE in a somewhat more comfortable position.

Deutsche Bank: BoE To Maintain A Neutral Bias.

The BoE face a continuing trade off, with data momentum remaining resilient at the same time as spot inflation prints are expected to accelerate over Q1. Market pricing has moved increasingly hawkish, with just over 50% of a 25bp hike priced by year end, but the MPC are likely to continue to stress downside risks while retaining a neutral bias as they allow Gilt QE to expire. From a technical perspective, the Bank will also publish a new market notice for the next Gilt re-investment. We see a growing risk that changes to the basket structure will soon be due, which would impact the medium basket in particular.

TD: BoE On Hold; GBP Rebound Temporary.

We have removed the rate cut from Q4 2017, and now look for the BoE to keep rates on hold through 2017-2018. We still see a strong possibility of a rate move over the next two years, but view the probability of either a hike or a cut as sufficiently high as to prevent us from ruling one out and choosing the other as our base case view. Until the UK outlook becomes clearer, we choose the middle road for rates. FX Strategy: Sterling has seen a moderate rebound as the UK economy remains resilient and some Brexit risks have diminished. With the GBP’s underlying fundamentals still vulnerable, however, we think this is only temporary and expect the downtrend in GBPUSD to resume in the weeks ahead.

Copyright © 2017 eFXplus™Original Article