Fundamental Forecast for Euro: Neutral

– The Euro was smacked with reality this week when 2013 German GDP came in at +0.4%.

– Incoming January PMI figures offer little reason for enthusiasm.

– Monitor the Euro’s intraday momentum with the Strong/Weak app.

The Euro was the second worst major performer this past week, losing -0.95% to the top US Dollar, while gaining only against the beleaguered Australian Dollar, by +1.44%. By no means was this severely negative for the Euro, but no longer are the positive fundamental drivers providing the same spark – namely speaking sustained low Italian and Spanish yields and a lack of deflation appearing in regional CPI readings.

The past week showed signs of the hope and optimism that has helped carry the Euro starting to crack. It was a stark reminder that the Euro-Zone remains mired in a period of stagnation when the final 2013 German growth reading showed that the Euro-Zone’s largest economy only grew +0.4%. Euro-Zone inflation remained near multi-year lows in December (core at +0.7% (y/y) unch), showing that demand across the region remains weak. Neither screamed “buy the Euro.”

These data aren’t necessarily surprising: the policy of diminished government spending and higher taxes (“austerity”) creates a difficult environment for consumers and businesses alike. Market participants simply may be overstimulated by the ‘abstract’ reasons to be long the Euro – a shrinking European Central Bank balance sheet, especially relative to other major central banks (namely the BoJ and the Fed) – as near-term growth data loses its luster.

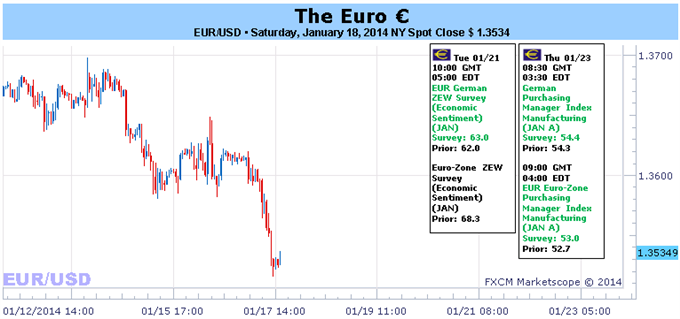

Certainly, the data due over the coming week paints a similarly improving yet unenthusiastic picture. On Tuesday, the January German ZEW survey is expected to show the highest Current Expectations reading (63.0) since March 2006 (63.4). This optimism may suggest that the Euro-zone’s recovery remains on pace, but in context of how the German economy performed last year these hopes have yet to fully translate into tangible reality.

The same can be said for the incoming PMI surveys due out on Thursday. Both the German and the broader Euro-Zone figures are expected show improvement across the board – in the Manufacturing, Services, and Composite indexes. Perhaps most interesting to watch – and what arguably jumpstarted Euro weakness at the beginning of the year – would be the French PMI surveys. The December figures showed a harrowing situation for early growth and labor prospects at least in the first half of 2014, a developing thorn in the side of the Euro as its second largest economy sputters.

As we’ve noted previously, it’s going to take a little more than some soft non-German data to provoke the ECB to do anything in the slightest. The November policy decision best exemplified this: only after German CPI showed consistent disinflation/deflation did the ECB act. The best reason for further easing from the ECB would be low excess capital levels – well-below the levels that prompted LTRO1 in December 2012. Nevertheless, with the positivity around the Euro morphing into a more neutral tone, we choose to take a more neutral outlook for the week ahead in absence of convincing positive or negative data due. – CV

To receive reports from this analyst, sign up for Christopher’s distribution list.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx