Euro’s Ugly Fundamentals, Italian Election Dent Optimism

Fundamental Forecast for the Euro: Neutral

Dollar, Yen Lead as Euro Snaps Back to Reality; EURUSD Under $1.3200

Euro Weakens on Growth Forecasts, LTRO News

US Dollar Up vs Euro, Pound After Fed Minutes; USDJPY Nears ¥94

The Euro struggled this past week, only outpacing the British Pound and the Canadian Dollar, while losing significant footing versus the Australian Dollar, the Japanese Yen, and the US Dollar. As noted the past several weeks, there have been unsettling political concerns arising at a time when market participants are beginning to look past the European Central Bank’s shrinking balance sheet via the LTRO repayments; this ‘double tap’ has led the Euro from its high on the first trading day of the month to its lows by the close of this week.

With respect to the EURUSD specifically, the shifting fundamental trends have been complimented by a technical breakdown as well. The recent decline has seen the EURUSD below both the ascending trendlines off of the December 2012 and January 2013 lows, as well as the ascending trendline off of the July 2012 and November 2012 lows, at 1.3260/80 and 1.3200/20, respectively. And when we consider the technical breakdown alongside the fundamental story propelling the EURUSD, there are many similarities. It is the convergence of both the fundamental and technical pictures that lead us to a ‘neutral’ bias for the coming week.

The two major themes over the past seven months – the duration of the EURUSD’s uptrend off of the July 24 low at 1.2041, when ECB President Mario Draghi said the central bank would do “whatever it takes” to save the Euro – have been: the ECB’s OMT program, which has led to an artificial compression of Italian and Spanish sovereign bond yields (especially on the short-end), dampening the financial aspect of the sovereign debt crisis; and the Federal Reserve’s willingness to oversaturate the economy with liquidity via its $85B/month in asset purchases, in an effort to foster full employment amid steady price pressures.

But now, as the EURUSD has broken from its seven-month long uptrend, these themes are disappearing: even as Euro-zone banks repay the LTROs, political issues in Italy – elections that could reinstall Silvio Berlusconi into the premiership – and Spain – evidently rampant corruption throughout the government – are shaking confidence; and the Fed’s January meeting Minutes suggest that the pace of the $85B/month in asset purchases is likely to dwindle sooner rather than later, as systemic risks increase and the US economy improves. All of the sudden, the tables have very much turned: the Euro had gained +3.28% against the US Dollar in 2013, through February 1; now it is up by +0.01%.

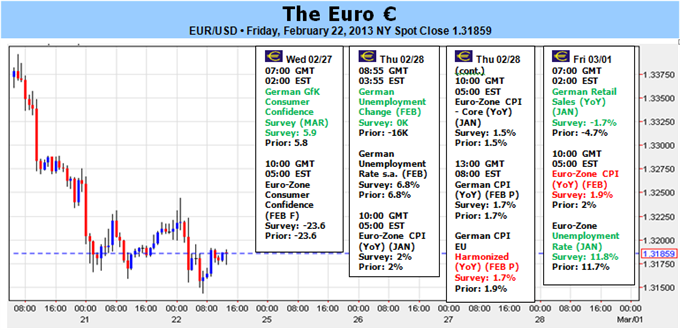

With the major themes shifting, the secondary influences are in the spotlight: the Euro-zone’s rapidly deteriorating growth picture. 4Q’12 GDP figures from Germany, France, Italy, and Spain were well-below expectations; and recent PMI figures suggest that the region’s recession, which has reached the levels last seen at the depths of the 2008 to 2009 financial crisis, could continue through the 3Q’13. The coming week should highlight the weak growth environment. On Thursday, the Euro-zone Consumer Price Index (JAN) should show deflation picking up on a monthly-basis, while both the headline and the core year-over-year readings should display price pressures at or below the ECB’s preferred +2% y/y pace. On Friday, the Euro-zone’s labor market reading is due, with the Unemployment Rate (JAN) forecasted to tick to an all-time (the wrong kind of record to set), according to a Bloomberg News survey.

While the negatives are abundant, a silver lining exists. Actually, two do. First, Silvio Berlusconi could lose the Italian election, set to take place between Sunday and Monday. A defeat of Berlusconi would be Euro-positive. Secondly, the US budget sequester comes into effect on Friday. If the end of December was any indication of what could happen, the Euro could find appeal – assuming Berlusconi loses – against the US Dollar once again, as focus shifts to negative influences on the US Dollar. It’s for these reasons that we must hold a ‘neutral’ tone this coming week. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx