Dollar Will Reengage Taper Speculation with FOMC, GDP and NFPs!

Fundamental Forecast for US Dollar: Bullish

Fed reporter Hilsenrath revives the market’s appetite for Taper speculation

Bloomberg and Reuters surveys show half of economists still expect a September Taper

Dollar and Stock Market at reversal risk

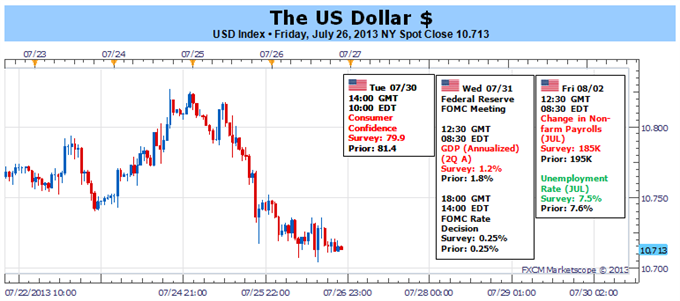

The Dow Jones FXCM Dollar Index (ticker = USDollar) dropped for a third consecutive week through this past Friday as volatility leveled off and ‘Taper’ concerns eased during a lull in the economic docket. This period of calm will come to an abrupt end this week though as a round of critical event risk will stoke the fires of stimulus speculation and generate heavy waves for risk appetite and the greenback. With a combination of the first reading of second quarter (2Q) GDP, July nonfarm payrolls (NFPs) and the Federal Reserve’s July rate decision; we is certain to see meaningful sea changes in the market’s most important fundamental theme: risk appetite.

It is important to recognize the importance of the Federal Open Market Committee’s (FOMC) monetary policy plans. Using the US equity index the S&P 500 as a benchmark, investor appetite continues to scale ever greater heights despite notable gaps in the fundamental backdrop. With the market’s favorite speculative asset class at record highs, we should be skeptical of jumping in on the exuberance when US and global growth is mundane, business revenues are slowing, unemployment is still high and investment returns are still exceptionally low. This is stark contrast between the traditional elements of economic strength and the incredible performance of capital markets. That disparity is filled by the temporary removal of perceived risk through the Fed’s stimulus efforts: a large safety net.

Yet, the central bank’s massive $85 billion-per-month purchase of Treasuries and mortgage-backed securities (MBS) will not last forever. Though we have yet to reach the Fed’s 6.5 percent target for the jobless rate, that is the level at which the discussion turns to tightening. Slowing the pace of the ballooning balance sheet (the Taper) begins before that threshold is reached. And, the market is comprised of forward-looking investors and speculators. The first step towards curbing support will be a concern for a market that has positioned itself in excessively risky assets (like high-yield corporate debt and Emerging Market assets) while employing record leverage (as evidenced by use of borrowed money amongst brokers on the New York Stock Exchange).

With the knowledge that the balance of optimism in the global capital markets is critical and that the Taper is perhaps the most catalyzing threat to this delicate conditions, we can grasp just how important the heavy round of event risk this week is.

Though there are quite a few indicators and events from the US and across the globe that can touch upon sentiment, the weight of three particular catalysts will drown out most other developments. Conditions will reach a boil by Wednesday when the 2Q US GDP release is due. Looking through the Taper/Risk filter, it is understood that the mandates of monetary policy (full employment and stable inflation) aim to support economic activity. The primary question currently troubling investors is whether the central bank will move to first Taper at the September meeting – which approximately half of economists polled by Reuters and Bloomberg this past week believe – or if data has necessitated more time at the peak stimulus pace. The 1.0 percent annualized rate of growth established by the consensus forecast would mark a significant slowing from the previous quarter. However, a mere moderation of pace would not likely alter the Fed’s plans.

Many people believe that stimulus will simply remain – or be expanded – to help drive growth and the recovery in labor markets. Yet, it is important to recognize that there are costs related to the effort. Given the tame PCE figures, inflation is a secondary concern. The risk of destabilizing the capital markets as investors recognize excessive levels of risk and exposure is far more pressing. Therefore, we have to look to the Fed rate decision later Wednesday to gauge exactly how confidence/concerned the group is about the need to build a possible bubble in order to reach a point of self-sustaining economic expansion. Few people believe this meeting will bring with it the Taper as the September event will offer updated forecasts and the Bernanke press conference (ideal for explaining difficult policy moves). Though a low probability, be wary of a possible Taper. More likely, the market will be reading the statement for clues on September.

Given the recent pullback in the dollar and retrenchment from traditional risk assets, it is likely that the market has given more weight to a deferred Taper. That being the case, a Fed statement that is unchanged in tone and rhetoric can set the currency into a rally and sentiment into a dive. The outcome of the Fed decision is critical to deciphering how the NFPs will be interpreted Friday. If the group backs off the pressure to curb stimulus, the data will carry less influence. If, however, September is still circled on the calendar…– JK

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx