Yen Would Benefit from Softer US Yields, but FOMC Turned Risk “On”

Fundamental Forecast for Japanese Yen: Bearish

The Japanese Yen was primed for strength against the US Dollar if the Fed tapered minimally…

…but ultimately the non-taper provided a major spark to risk assets globally, sinking the Yen against high yielding FX.

Last week’s COT data showed speculators piled into short Yen positions ahead of the Fed.

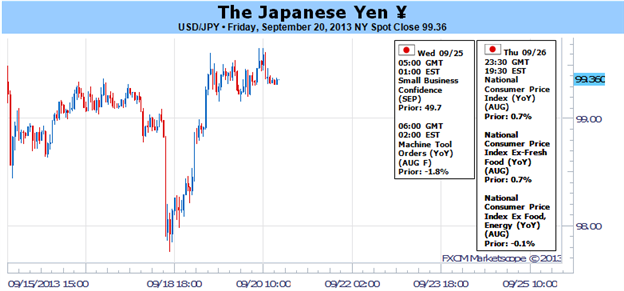

The Japanese Yen was a bottom performer over the past week, losing ground quickly from Wednesday forward after the Federal Reserve surprised investors by keeping QE3 in place at its current $85B/month pace. Market participants were widely positioned for the Fed to taper QE3 by $5B to $15B, which we speculated could provoke a retrenchment in US yields, to the Yen’s benefit. While this proved true for the US session on Wednesday after the Fed meeting, the non-taper proved to be a major catalyst for “risky” assets. This theme should remain prime as the Japanese economic

With the Fed maintaining QE3 at $85B/month, emerging market and commodity currencies (high yielding/high beta FX) surged between Wednesday and Thursday, to the Yen’s detriment. Perhaps for good reason, too: Japanese yields plummeted to their lowest level since early-May, transforming the Yen not as a vehicle to benefit as a safe haven but as a funding currency amid a swell in central bank-fueled exuberance. It is likely that the Yen suffers against higher yielding FX over the near-term.

The decision to not taper QE3 in September leaves the Yen in a precarious position going forward. Foreign concerns remain hazy but look to be steadying. Geopolitically, international consensus is growing to avoid military conflict in Syria now that the Assad regime has begun cooperating with weapons regulators. In Iran, a stage for more open dialogue with the West has potentially emerged in new President Hassan Rouhani. Regardless if these talks for broader cooperation amount to anything, there’s reason to believe the “war premium” built into commodity markets (particularly oil) and the USDJPY (via Treasuries) could thaw.

Out of the United States, two potential catalysts exist to knock the Yen around: the Fed, of course; and Congress. The Fed made it quite clear that rhetoric aside, incoming economic data would need to improve for the Fed to taper QE3. This is the same line that was towed at the June FOMC meeting which kick started the ‘Septaper’ speculation. The case for why the Fed chose not to taper was easily made with a glance towards inflation and labor data, which hadn’t shown progress since June. It also means that there is increased influence of US data on currencies and interest rates; the USDJPY in particular should show increased sensitivity to labor and inflation data.

The US Congressional influence on the Yen should become increasingly profound over the next few weeks as it appears that another debt limit showdown is likely. As long as Congress remains a veritable drag on the US economy – Fed Chairman Bernanke aptly pointed this out on Wednesday as a reason that the Fed didn’t taper – there is scope for the Yen to at least remain buoyant against the US Dollar. The upcoming votes on the continuing resolution bills in the House and the Senate will shape the debt debate; if they don’t go smooth, greater turbulence in October is likely. In such a case, the Yen’s misfortune against higher yielding FX would quickly turn, just like in August 2011.

At home in Japan, influences are neutral on the Yen as the economy is generally better than previously expected. The sales tax hike appears to be a go, with Prime Minister Shinzo Abe set to decide the matter on October 1, and the Bank of Japan has thus far indicated that it would be willing to extend further monetary easing to prevent a dip in economic activity (higher taxes lead to lower consumption).

The government has pressed firms to raise wages to help offset the matter as well (which would balance out lost consumption), but so far little progress has been made on this front. Even if Japan is successful in stoking inflation, without wage growth, consumption will fall (consumers will have reduced purchasing power), and the economy will suffer once more – putting Abenomics itself at risk for total failure – and potentially ushering in greater concerns about Japan’s seemingly insurmountable debt burden. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx