Fundamental Forecast for Japanese Yen: Bullish

– As likelihood of sales tax hike increases, so too does additional stimulus from the BoJ.

– Sabre-rattling between Russia and the United States peaked on Friday, driving demand for safety.

– Use the DailyFX Calendar App to track all of the key events impacting the Yen this week

Investors are losing faith in the Japanese Yen, and not even a late-week rush to safety could lift the funding and safety currency out of the FX cellar. The Yen was the worst performing major currency last week, shedding a whopping -4.52% and -4.18% to the New Zealand and Australian Dollars, respectively, and even slipping by the recently downtrodden Swiss Franc by -0.10%. Certainly, the rebound in emerging markets helped drive the return to risk, as the Asian Dollar Index (ADXY) rebounded by +0.41% this week after sliding by -2.15% in the 2Q’13 (a notable drop in context of the ADXY’s high to low move of -4.55%).

With emerging market financial hotspots showing signs of cooling, it was natural to see the Yen lose a step or two given its role as a liquid, safe currency. But it wasn’t just exogenous tensions being relieved; indeed, an evolution of the sales tax debate at home drove the Yen lower.

The Bank of Japan kept its policy on hold this week as expected, but it was commentary after the meeting that help stoke the USDJPY rally above ¥100.00 for the first time since late-July. BoJ Governor Haruhiko Kuroda noted on the sales tax debate that if the fiscal tightening measure – intended to combat the nation’s rising debt burden, which just passed the superficially important ¥1 quadrillion mark – provoked economic weakness, that the BoJ would consider further easing policies to help boost demand once more.

For weeks we have suspected that the eventual approval of the sales tax hike could stoke more easing, first noting that its initial diminished chance served as a bullish catalyst for the Yen; and then more recently that a sales tax hike would reduce pressures on inflation, thereby setting up for future BoJ action. With Governor Kuroda now making this sentiment public, we are paying extra attention to this fiscal policy debate over the next coming months as it evolves.

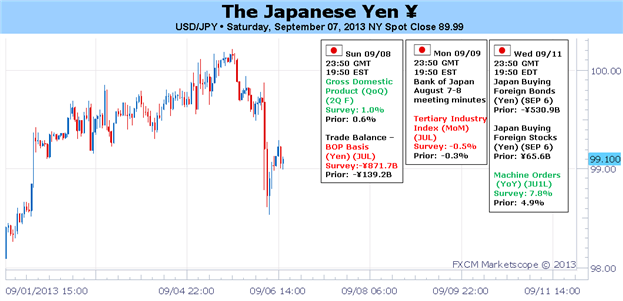

Accordingly, with the domestic tone shifting for Japan, it will be necessary for incoming growth and inflation data to remain buoyant in order for the Yen to enjoy further reprieve. This week, the final 2Q’13 GDP report will be released; and the downward revision is expected to be reversed.

The final reading should show that the Japanese economy, the world’s third largest, grew by +3.9% annualized versus +2.6% previously reported, while quarterly growth is seen higher to +1.0% from +0.6%. Both these revisions higher would see the economy performing above the first readings of +3.8% annualized and +0.9% quarterly. A potential setback in data this week could be the dramatic trade deficit expected for July, at -¥862.4B from -¥139.2B – but we expect officials and market participants to dismiss the gap due to higher energy costs, not a Yen that is too strong.

With the August US labor market report roundly disappointing, the expected readings for 2Q’13 GDP growth could provide ample fundamental footing for the Yen to turnaround in the near-term. Unrelated to economic data, further tensions between Russia and the United States over Syria will also support the Yen. As seen in illiquid market conditions on Monday and then again during the G20 summit on Friday, the Yen stands to be the preferred safe haven in FX markets during times of geopolitical upheaval. While we remain long-term bearish on the Japanese Yen, domestic data and exogenous events do not warrant a bearish bias; we are open to an upside surprise. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx