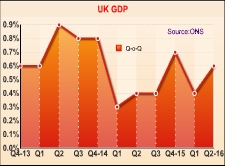

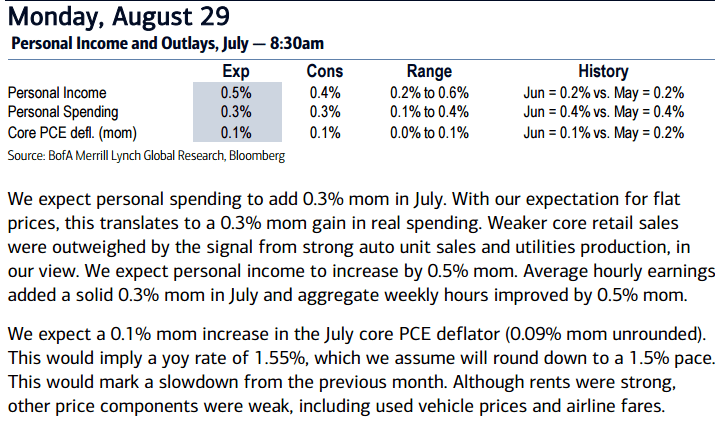

We have taken off all short GBP exposure* for now as the short positioning became extreme and the UK economic data have been surprising to the upside relative to the US. The BoE's easing policy was important for our bearish GBP call too as GBPUSD is highly correlated with the performance of UK gilts (Exhibit 4). GBPUSD has diverged slightly from the 10y gilt yield since the release of strong UK retail sales, suggesting that the rally has been position reduction rather than a change in fundamental views. The underperformance of the USD side of the pair could also allow GBPUSD to rally much beyond the initial resistance around 1.35.

Weak GBP doing its job: Another reason to be less bearish on GBP for now is that it appears that the cheaper currency is already doing its job of attracting foreigners into GBP assets. Retail sales rose by 1.5% in July, driven largely by an increase in the number of tourists who were buyingnon-food items.Luxury goods retailers, like those selling Swiss watches,are already seeing a pick-up in spending, particularly as prices haven't been increased across the board. We will be watching consumption-related data in coming weeks to see if the strength continues.Foreign corporates are on a UK spending spree too. Exhibit 5 shows that announcements of M&A into the UK have reached £40.7 billion in 3Q already, only a fraction lower than the average for the past few years. The latter is only currency-supportive if the purchase is made using cash in a foreign currency. The BoE's corporate bond purchase programme is incentivising corporates to issue GBP debt, which, if used to make an acquisition, would reduce the currency supportive impact.

What could make us sell GBPUSD again? Very strong US data causing markets to change their perception of the pace of US rate hikes in the coming year could make the USD rally across the board. In contrast, if UK economic data, particularly services production, were to show a large contraction, markets may assume the BoE will need to ease more to help corporates. The markets are pricing in a small chance that Article 50 won't be triggered at all, and only a moderate chance it will be triggered this year. Should the government strongly indicate that Article 50 will be triggered this year, then this could mark a turnaround for GBP. Finally,any signs that the November Autumn statement may limit fiscal spending would be GBP bearish.

These trades were recorded in eFXplus Orders

Copyright © 2016 Morgan Stanley, eFXnewsOriginal Article