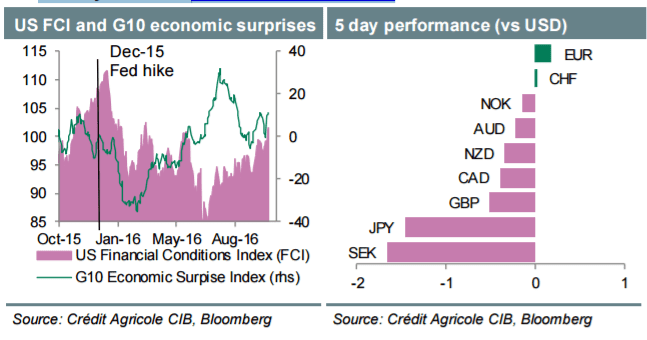

Investors have several reasons to worry about a potential taper tantrum. Indeed, the next Fed hike is drawing near (we think December rather than November); concerns about a BoJ and ECB taper linger, and stabilising commodity prices are supporting realised and expected inflation across G10. The fear is that an aggressive fixedincome selloff accompanied by a bear steepening of global yield curves could trigger a spike in risk aversion. Coupled with intensifying demand for USD-funding into year-end, this could spell out trouble for less liquid, risk correlated G10 currencies and liquid USD-proxies like EUR and JPY.

We believe that any taper tantrum angst is premature, however. Next week’s Fed meeting should make an explicit reference to a rate move in December but there seems to be less scope for aggressive tightening of US financial conditions given that the implied probability of a hike is already close to 75%. We doubt that there will be a sustained risk selloff either, especially if the non-farm payrolls and ISM data underpins the constructive outlook for the US economy and adds to the recent stream of positive economic surprises from around the world. Next to the Fed and US data, more evidence of growing demand for USD-funding, reflected in widening of EUR-USD and JPY-USD cross currency swap rates, and elevated USD/CNH rates, should keep USD supported.

The BoE’s inflation report should attract some attention next week, not the least given that some analysts are still calling for a rate cut. We expect the MPC to keep policy unchanged and link any prospects of further easing to the path of the GBP, which according to Governor Carney has depreciated ‘substantially’ more recently. Data releases as well as indications that the UK government would pursue a somewhat ‘softer’ version of Brexit could also help GBP consolidate more broadly in the coming days.

Also, next week, we expect both the BoJ and the RBA to keep their policies unchanged. The former should alleviate recent market concerns about an imminent taper that was fuelled by a drop in the 10Y JGB yields to below zero. This together with the persistent steepness of the JGB yield curve should keep Japanese stocks and USD/JPY generally supported. The RBA could revise up its inflation outlook and dash hopes for further easing from here, helping AUD regain more ground. Demand for carry trades could continue to support the AUD in the absence of sustained tightening of global financial conditions. We recently entered a tactical long in AUD/JPY.

Credit Agricole's FX Trading Targets & Views Continuously Updated on eFXplus Orders & Forecasts

Copyright © 2016 Credit Agricole CIB, eFXnews™Original Article