The US Dollar struggled to close in the positive last Friday, after a softer than expected US GDP reading for the 4th Quarter that was now confirmed at 1.9%. We also had durable goods orders for December which continued to contract despite expectations for an expansion. Risks of slower economic growth and concerns over Trump’s trade policies left its toll on US treasury Yields as well.

The US Dollar index, showing the strength of the USD against a basket of other major currencies, is in negative territory this morning. Current price levels of 100.27, make it look like its a matter of time till we have another retest of 100 levels. 99.80 has acted as a horizontal support since last Monday.

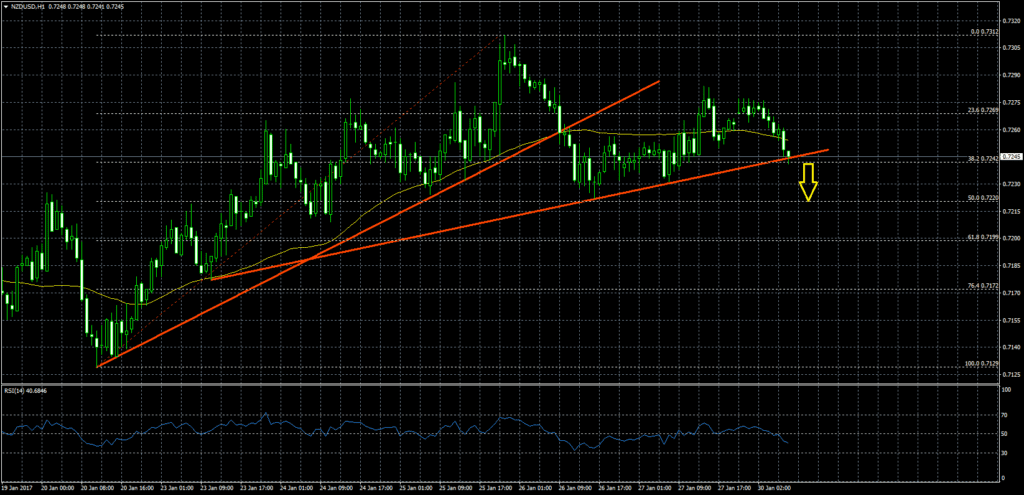

EURUSD closed higher on Friday and has also gapped higher this morning, however gains have so far been relatively modest, with the single currency lacking the necessary motivation despite taking advantage of the softer USD.

Asia is quieter than usual as China and Hong Kong amongst others are closed for holiday.

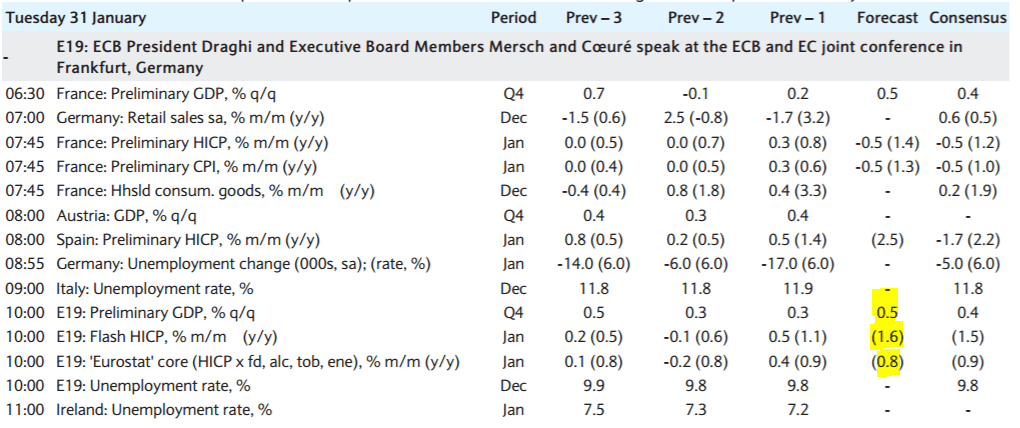

Later this afternoon we shall get a glimpse of German CPI for January, the Y/Y figure is expected to tick slightly higher to 2% from a previous 1.7%.For the rest of the week we have BoJ Monetary Policy Statement, German Unemployment, EZ & Canadian GDP on Tuesday; US & Chinese Manufacturing PMI & FOMC rate decision on Wednesday; BoE Rate Decision on Thursday; and US NFP on Friday.