USD: Verbal Intervention Poses Near-term risks. Neutal.

Given the increased focus from Trump officials on the strong USD, we think it may be difficult to trade USD from a short-term perspective. Administration comments risk other countries turning towards a more hawkish monetary policy and pushing their currencies higher. China may already be an example of this. However, we don't like selling USD given broadly improving data. The closing output gap should win out in the long term in pushing USD higher but, for now, we turn neutral.

EUR: Periphery in Focus. Bearish.*

Widening EMU peripheral spreads are going to be difficult to contain without reduced political volatility or the ECB keeping monetary conditions extremely loose. With inflation rates remaining widely different across the Eurozone members, the ECB may need to set monetary policy for the weakest link, causing the loose policy to limit the upside for the EUR. That said, the USD side is expected to become more volatile and needs to be watched closely.

JPY: Downside Risks Increasing. Neutral.*

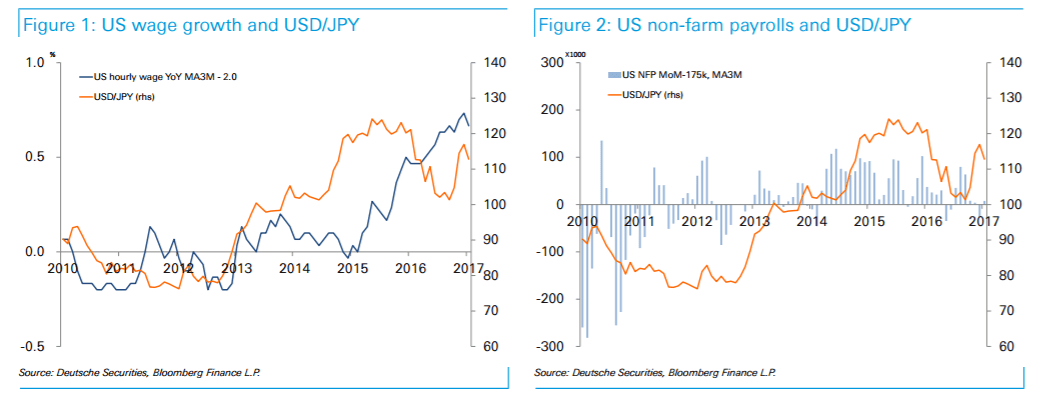

We expect USDJPY to rise in the medium-term but believe it is increasingly at risk of falling in the short-term due to comments from the Trump administration and risk of protectionist measures. If the reflation trade reignites, we think JPY is the best short as the BoJ's yield curve management ensures that Japan's yields remain relatively low. We are watching tomorrow's rinban operation closely to see if the BoJ reinforces this policy as 10yryields have risen to their highest level since the policy was implemented. Failure to combat the rise in yields may indicate that the BoJ is turning more hawkish as a way to appease the Trump administration's concerns about the weak JPY.

GBP: BoE Not Hiking Yet. Bullish.

The BoE's inflation report offered investors information that they largely knew: inflation is on the rise and consumption has been strong. Going forward the consumption – real wage dynamic will be watched closely. A slowdown in consumption would lead the MPC to loosen policy. We keep our long GBP/JPY position for now. We are looking for long term opportunities to buy GBP/USD.

CHF: Peripheral Spreads Drive CHF. Neutral.

We continue to expect the SNB to limit the downside for EURCHF in the short term. In times of market uncertainty in the Eurozone and peripheral spread widening, we would look to sell EURCHF as a political hedge. We are not looking to buy USD/CHF, even if it has moved to more desireable levels.

CAD: Fade CAD Strength. Bearish.

We continue to believe recent CAD strength will unwind and like trading CAD from the short side. First, the market hasn't priced in the very dovish BoC from last week and needs to price a flatter curve. Second, the CAD is not priced for any meaningful chance of trade protectionism but will be heavily impacted if border adjustability is enacted. Third, Canada's economy has not rebounded in line with the US and Canada's output gap is widening. We don't expect CAD to benefit much from the Keystone pipeline or small changes in oil prices. Poloz's comments this week echoed these points, saying the rise in CAD is premature given excess capacity and that the BoC doesn't expect to be following the Fed right now.

AUD: Short-Term Risks to Bearish View. Bearish.*

We are medium term AUD bears but acknowledge short-term risks driven by a potential weak USD and better AUD trade data. Still, Australian domestic data has disappointed, including 4Q CPI, as the rest of G10 has seen improving data. Meanwhile, China's interest rates have been rising as the PBOC attempts to manage leverage in the property and bond markets, reducing growth expectations and growth in the property sector (important in its linkages for Australia). Lastly, AUD valuation is getting to more extreme levels, particularly with where yields have gone since the US election. It is possible we see some pushback from the RBA on this pricing at the upcoming meeting.

NZD: Outperformance vs AUD. Neutral.

We still see the NZD outperforming the AUD, with last week's positive CPI print, signs of increasing immigration, and expectations for a strong dairy auction supporting NZD. We don't see RBNZ pricing as extreme right now and despite NZD TWI strength, expect the RBNZ could remove its easing bias at this week's meeting. Ultimately, NZD will be vulnerable to any fall in risk appetite or a downturn from China but still less so than Australia (whose domestic picture is also weaker).

*These trades are recorded and tracked in eFXplus Orders.

Copyright © 2017 Morgan Stanley, eFXnewsOriginal Article