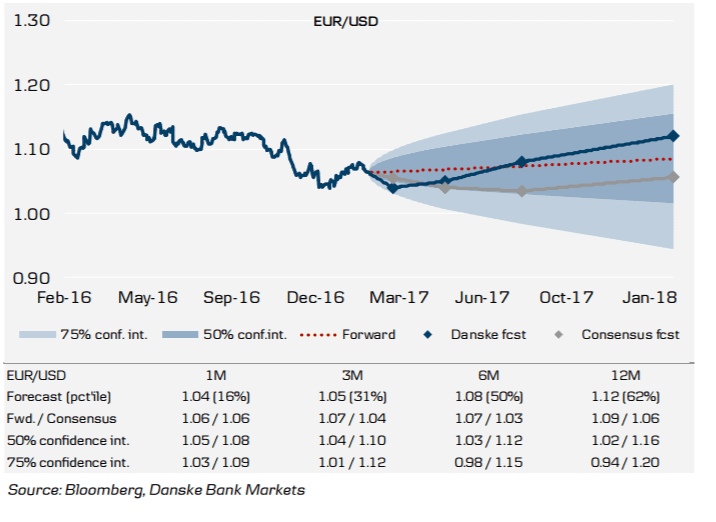

We remain bullish on the dollar expecting the euro and yen to trade in weaker ranges of 1.00-1.10 and 115-125 this year.

First, US data flow remains consistent with the Federal Open Market Committee hiking interest rates three times in 2017. January’s employment report showed payrolls rising by 227k. Though revisions shaved 39k off the prior two months’ payrolls, current job gains are ‘well above the pace of 75,000 to 125,000 per month that is probably consistent with keeping the unemployment rate stable over the longer run’ as Fed Chair Yellen observed in her January 19 economic outlook speech.

Second, Fed officials continue to see further rate rises this year. The January 31-February 1 FOMC statement was little changed from December’s. But policymakers acknowledged the improvement in ‘animal spirits’ seen since November’s elections by adding the line ‘measures of consumer and business sentiment have improved of late.’ Short term rates markets have little priced for the next FOMC meeting on March 14-15.

Third, market expectations for near term fiscal loosening may have ebbed as the White House and Congress negotiate on border adjustment and corporate and income tax policies. But if the Trump administration finds agreement with the Republican leadership in the next few weeks, the dollar, stocks and Treasury yields will rally sharply again. The new president is due to give a state of the union address on February 28.

Last, the Trump administration’s latest immigration policies are unlikely to lead to a sharp re-allocation of Middle East funds away from the US as occurred in 2002 after the Bush administration’s response to the September 11 2001 terror attacks. The new restrictions on arrivals from seven Middle East and North African countries did not include citizens from the largest holders of capital in the region – Saudi Arabia, Kuwait, Qatar and the United Arab Emirates.

The main risk in the near term for dollar bulls remains the lack of a clear, near term catalyst from either the Fed or the new US administration to spark a new round of greenback buying.

The next key events will be Yellen’s ‘Humphrey-Hawkins’ testimony on February 14-15 and the FOMC minutes on February 22.

Copyright © 2017 RBS, eFXnews™Original Article