US Dollar on Cusp of Bullish Trend Revival, Focus on S&P 500 and GDP

Fundamental Forecast for US Dollar: Neutral

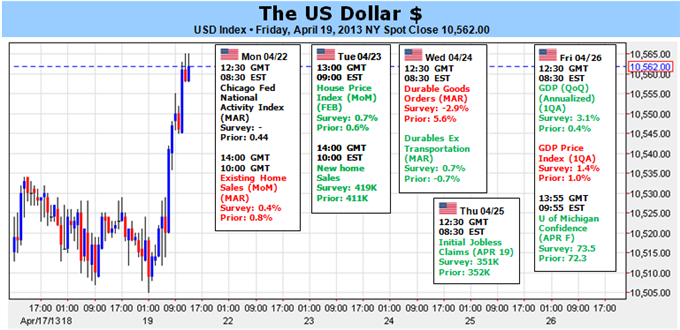

USDollar approaches 10,600 while USDJPY closes in on 100

Balance of Fed officials’ outlook tipping towards a downshift in stimulus

Safe haven dollar and risk effigy S&P 500 risk break at key levels

We have been here multiple times over the past weeks and months. Conditions align for a market-wide shift in risk appetite that could catalyze the dollar higher, yet the spark that can set everything in motion remains elusive. The opportunity this time around has not yet been snuffed out, but the market has shown us the threshold for progress to a committed trend can be exceptionally high. That can be a problem as we don’t have a clearly defined theme that can alter the entire face of risk the world over. That said, the interest in a number of themes – the timing of the Fed’s QE3 wind down, systemic volatility in exchange rates through competing stimulus programs, global growth forecasts and a possible US slowdown amongst others – could finally put these markets in motion by brut force alone.

First and foremost, we should appreciate the clear potential behind the currency. Looking at the Dow Jones FXCM Dollar Index (ticker = USDollar), we see the greenback ended Friday at 10,564 – technically the highest close since August 31, 2010. However, the currency hasn’t convincingly overtaken last month’s swing high; and the midpoint of the past five year’s range stands tantalizingly at 15,565. The same proximity to major breakouts is seen in the most liquid of the dollar’s major pairings. EURUSD has turned to congestion just above 1.3000 and USDJPY stands below the instantly recognizable 100 figure.

Though there is a magnetism to these impressive technical levels, establishing a committed trend requires a strong fundamental drive to align the mass’ trading intentions. Without doubt, the most influential ember would be a shift in sentiment itself. There is no more powerful force in the market than the balance between fear and greed. As the world’s reserve currency, the dollar’s appeal builds the closer the barometer moves towards panic. We have already seen volatility indexes – considered ‘fear’ gauges – put in for a measured trend shift higher and the correlation between different asset classes (currency, equities, commodities, bonds) revived. An ideal signal for pessimism’s usurping the bulls’ control would be a collapse from the S&P 500 below 1,535.

The US equity market reflects not just the most familiar investment vehicle – a critical characteristic for a sentiment measure – but it is also a symbolic manifestation of the confidence in central bank stimulus. The artificial withdrawal of perceived risk by the Federal Reserve and other global central banks encourages market participants to tolerate tepid returns on perilous investments. That brings us to an important but generally underappreciated topic of the speculative ranks – forecasting the end of the QE3 program. The FOMC minutes of the past week revealed a growing consent to easing back on the expansive $85 billion-per-month program. That doesn’t mean that the Fed will come to a full stop on the program in the immediate future – much less shift to rate hikes – but speculation will start to price that eventuality in well ahead of time.

Moving forward, speeches given by US central bankers will sway a more attentive crowd and data will be judged for its ability to put the medium-term forecast for a 6.5 percent jobless rate and 2.5 percent inflation rate (the Fed’s confirmed targets) within sight. In the week ahead, the 1Q US GDP report will carry a lot of weight in this tenuous balance. Should the economy’s activity hold up despite the tempered pace of its global counterparts, it could be considered a sign of the region’s resilience and the diminished need for stimulus. That said, a disappointment is unlikely to present an immediate escalation in support and could still spark risk aversion along traditional routes.

There are a number of other indicators and events that can stir other themes, but the burden of trend development must always come back to ‘risk trends’ for the kind of move that sends a tremor through the entire market. However, there is another aspect that is starting to present a more measured benefit to the dollar – the escalation of stimulus efforts from the Fed’s major counterparts. The BoJ has announced a remarkable program and the BoE is likely to upgrade. If the ECB were to join the fray and reverse its balance sheet reduction through early LTRO repayments, the dollar will gradually gain appeal. – JK

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx