Fundamental Forecast for Dollar:Neutral

Though the S&P 500 and yen crosses retreated Friday, it too early to call a full-fledge risk aversion move

NFPs keep the market’s time frame for the first Fed hike on track, stimulus expectations for others may offer more support

Have an opinion on the US Dollar? Trade it via Currency Trading Baskets

The US Dollar is a favored safe haven currency. That is a good role to play given the slide in US equities and other ‘risk’ benchmarks to close this past week. Furthermore, the market suspects the Fed is committed to deescalate its extraordinary QE3 program which sets a definable timeframe for the return to rate hikes. Both of these major themes seem to be moving in the greenback’s favor. Yet, to break months of trend and complacency, a greater level of conviction is needed than a mere bias. And, that is what could hold the dollar back from breaking below 1.3600 on EURUSD, 1.6500 with GBPUSD and generally developing a more substantial trend.

Starting – as always – with the aspect that carries the most market-moving potential, risk trends are without doubt the dollar’s most intense sponsor. When a pullback in capital markets escalates into a panic, the liquidity the currency represents (via Treasuries and money markets) drives capital through the exchange rate in waves. Yet, there is a broad intensity gap between a pullback and panic. At what level does fear solicit the world’s most liquid currency for harbor?

While equity markets’ tumble this past Friday (S&P 500 down 1.3 percent and the Nasdaq Composite 2.6 percent) was substantial, it has hardly built the breadth and momentum that normally represents a destructive deleveraging effort. Stock indexes are only modestly below record highs. Volatility measures show little demand for insurance or expectations of adverse market movement – however you want to read it. And, bouts of cross-asset ‘flight to safety’ have proven short-lived and have fallen well short of the intensity that revert the dollar to its primal state.

To generate the kind of anxiety that leverages the greenback’s liquidity over the diversification theme to the euro, the yield focus on the sterling, the carry trade unwind behind the yen; we need either a lasting ‘risk off’ run to infect the broader financial system or a spark that creates a severe market dislocation. From the docket itself, there are few scheduled events that present that boast that kind of influence. On the other hand, such shocks are rarely telegraphed or the progeny of simple data. Keeping track of the level of bearish pressure behind a benchmark – like the S&P 500 – and seeing the dollar revert to ‘safe haven’ against progressively better-balanced counterparts (emerging market currencies, NZD, CAD, AUD, GBP, EUR and JPY – in that order) is the best confirmation.

We are more likely to see progress from the dollar develop around interest rate expectations. While yields the world over are still extremely low and we are still one foot in stimulus programs, the FX market is forward looking. Should the market believe the US is due a rate hike before its counterparts, the rise in market rates and inflow of capital will follow. The US labor statistics for March released this past week reinforce the view already assessed by the market: maintaining the Taper through October or December and then the first FOMC hike by mid-2015. Payrolls were in-line at 192,000, unemployment held at 6.7 percent and the participation rate rose to 63.2 percent.

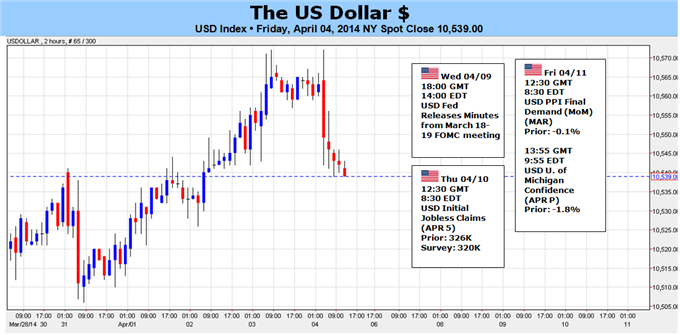

On the docket for next week, there are a few stand-out releases rate watchers should keep tabs on. The minutes from the FOMC’s March 18-19 meeting (which generated so much market response) can offer further insight as to what thresholds the group is implicitly following and their assumptions. Economic health will be measured by the University of Michigan Consumer Confidence survey, NFIB Small Business sentiment report and consumer credit statistics. Inflation, meanwhile, will see updates via producer and important price indexes.

And, given that this is a relative assessment; it is always important to assess the strength of the dollar’s largest counterparts. This is a particularly important evaluation against the euro and pound. Given the runaway capital inflow in the Eurozone and elevated rate forecast for the UK, a correction on their part could prove a substantial booster for the greenback. – JK

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx