Strong Data Could Boost the Buck’s Fortune into the End of March

Fundamental Forecast for US Dollar: Bullish

Federal Reserve’s March 2013 Economic Projections in One Word: Uninspring

USD Searches for Support Ahead of Fed Rhetoric, GDP Revision

US Dollar Turns Lower Anew – S&P 500 Hovers at Support

The US Dollar finished the week overall lower, althought it was not the worst performer; it outperformed three majors while underperforming the other four. In what proved to be a tumultuous week for the Euro, one marked by blustering words out of Cyprus that amounted to little more than hot air, the US Dollar saw both flowas a safe haven currency and as a growth currency, thanks to a cautiously optimistic group of Federal Reserve policymakers. The FOMC’s updated quarterly forceasts showed that the world’s foremost central bank is reeling in its growth projections for the US economy in 2013, though expects growth to be north of +2.0% overall.

Against the backdrop of cautiously optimistic, yet conservative economic forecasts, the US Dollar holds a bullish tone for the coming week, as the data set to be released will continue to paint the picture of an improving US economy. It is worth noting that the Cypriot bailout proceedings should also be kept on the radar. If they head ‘south,’ which would be denoted by the European Central Bank cutting off liquidity to Cyprus on Monday before the banks reopen on Tuesday, the US Dollar would undoubtedly be a top performer, though I suspect the Japanese Yen might outperform in that situation as the 2s10s Treasury yield spread compresses. However, with a tentative solution on the table thanks to a late-Friday vote by the Cypriot parliament, it is very possible that the bank run/liquidity fears materialize, thus removing a potentially potent accelerant for the US Dollar.

Nevertheless, because US Treasury yields have increased this year – often a sign of market participants pricing in stronger economic growth and/or higher inflation expectations – the US Dollar has embraced the hybrid role of both a safe haven currency and a growth currency, which is why the data due this week comes into focus: the Fed is encouraged by recent labor data, and their views would be vindicated, and the US Dollar would rally, if the significant data ahead even meets consensus expectations.

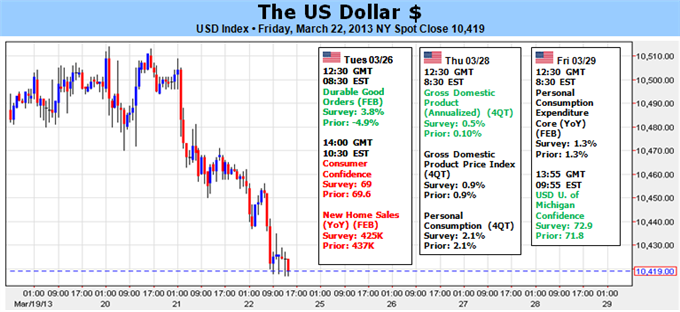

The major data is spread out among Tuesday, Wednesday, and Friday. To start, the February Durable Goods Orders report should show a sharp rebound, suggesting that US consumers are stepping up purchases of items with lifespans of three years or more – the “big ticket” items like home appliances or automobiles. A strong consumer is important for the US economy, with some 73% of headline GDP growth coming from consumption. The official government March Consumer Confidence gauge should show a slight moderation in sentiment, which wouldn’t surprise given the horrible preliminary March U. of Michigan Confidence report from last Friday.

On Wednesday, the final revision to the 4Q’12 GDP figure will be released, with an expected mark-up to +0.5% annualized, from +0.1% at the first revision, which itself was an improvement over the -0.1% figure initially released. Considering that defense spending plunged by -22% on an annualized basis in the 4Q’12, a half percent tick higher in overall growth is modestly impressive; government spending has plummeted the past several months, weighing heavily on overall growth. This is the most important release for the US Dollar this week, and could prove to be a major catalyst in either direction – we’re looking for a stronger buck.

The significant data ends on Friday, rounded out by February Personal Income and Personal Spending data, which too should speak to the resiliency of the US consumer. The bit of inflation data due out on Friday, the February Personal Consumption Expenditure Core figure, should show that prices pressures remain comfortably below the Fed’s medium-term target of +2.0% y/y; recall that “The Evan’s Rule” dicates that the Fed will end QE3 if either the Unemployment Rate falls to 6.5% or inflation rises above +2.5% y/y. After the opening bell, the final March U. of Michigan Confidence gauge will be released, with a slight revision higher expected. After the initial report produced the lowest sentiment reading in a year, this release could provide some late-week volatility for the US Dollar. The stronger the revision, the greater the positive impact on the US Dollar.

Overall, we remain fundamentally bullish, and the forecast has indeed improved to bullish alongside a (much-needed) relieved technical picture. Despite its troubles the past few weeks, the US Dollar remains a top performer this year, alongside the two highest yielding major currencies, the Australian and New Zealand Dollars, which it trails by -0.47% and -0.84%, respectively. Buying dips is favored. –CV

New to FX? Register for this free 20 minute course HERE and learn common FX terms like leverage and how to implement conservative amounts.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx