Sterling Boosted by Haven Flows Thanks to Cyrprus; Data Outlook Soft

Fundamental Forecast for British Pound: Neutral

Chancellor Osborne Presents 2013 Budget; Sterling Rallies on BoE Remit

Sterling Recovery Continues; Euro Stumbles as Data Diverges

The 8-Year Sterling Cycle

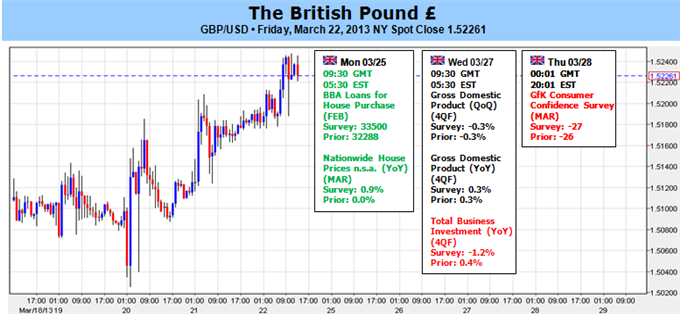

The British Pound was a top performer this week, trailing only the resilient New Zealand Dollar and the quizzically strong Japanese Yen, while adding +0.76% against the US Dollar, and +1.42% against the Euro. There were three main influences this past week for the British Pound, ranked in order of importance: Chancellor George Osborne not changing the Bank of England’s remittance to allow for higher price pressures; the BoE keeping the Asset Purchase Program unchanged at £375B amid further division in the Monetary Policy Committee; and the Cyprus crisis, producing the desire for a haven from the Euro. Yet, despite the bullish implications that these events had for the Sterling this past week, they will be much more tepid in the week coming; and against a soft data backdrop, we must take a neutral bias towards the British Pound.

On the BoE March meeting Minutes: the Monetary Policy Committee expressed significant concern over the British Pound’s rapid depreciation thus far in 2013, citing concerns that the weak fiat could trigger higher price pressures. Considering that fiscal policy remains firmly geared towards austerity – lower government spending and higher taxes – the British consumer is already facing an uphill battle (more on this below).

On the BoE’s unchanged remit: it should be noted that the GBPUSD was sliding throughout the course of Chancellor George Osborne’s 2013 budget presentation to parliament up until the moment he noted that the BoE’s remit would continue to call for a medium-term inflation target of +2.0% y/y. This reveals two key points: market participants aren’t particularly enamored with the changes to the UK’s 2013 budget; and that part of the Sterling’s weakness was rooted in speculation that the BoE would step up its QE program with fervor, leading to higher inflation and lower yields. The ‘relief’ provided that higher inflation wouldn’t be allowed means that purchasing power for the British consumer won’t be eroded as quickly, removing another potential hurdle for the struggling economy.

On Cyprus: the British Pound benefited against the Euro from mid-2011 through mid-2012 thanks to investors seeking to diversify out of the 17-nation common currency and into another within close geographical proximity. With the Swiss Franc’s safe haven duties mostly relegated to the sidelines thanks to the 18-month old EURCHF floor at 1.2000, the British Pound, like the Nordic currencies, has benefited as an ‘alternative safe haven’ of sorts. This proved true again this week, when the money laundering hub of Eastern Europe, Cyprus, flirted with leaving the Euro-zone over a deposit tax.

The mix of these factors proved slightly bullish for the Sterling, but if anything, they should be more muted going forward. The Cyprus situation proves to be the most worthy candidate to provoke further appreciation in GBP-based pairs, as the bullish fuel rooted in the BoE is likely to wane. Why? Fiscal policy remains tight; the newly-minted 2013 budget shows just that. Monetary policy will necessarily be used to offset any fiscal drag, keeping an implicit downside pressure on Gilt yields, and thus, the British Pound. As we’ve seen with the Bank of Japan and the Federal Reserve, more liquidity is the go-to policy tool; BoE policymakers won’t differ either.

A look at the economic docket this week shows that there are few important releases, nevermind that the calendar is far from saturated overall. The most significant data, the final 4Q’12 GDP revision on Wednesday, isn’t expected to show further positive momentum, with the triple-dip recession being confirmed. Recent Industrial Production and Manufacturing Product data has eroded as well, implying continuing growth weakness in the 1Q’13. Although the tone of the GDP revision is negative, because it is a final revision and thus well-known, it is priced into to Sterling at present time, and should have a minimal impact.

In summation, between soft economic data, diminished momentum behind recent shifting interest rate expectations, and the outside chance that something completely brutal results from Cyprus, we find it is best to take a neutral outlook on the British Pound for the coming week. – CV

New to FX? Register for this free 20 minute course HERE and learn common FX terms like leverage and how to implement conservative amounts.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx