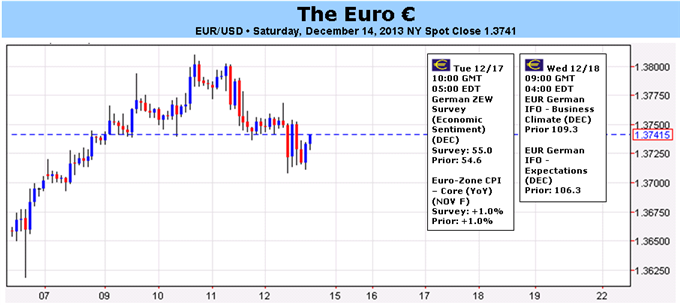

Fundamental Forecast for Euro: Neutral

– The Euro has remained generally supported after the December 5 ECB meeting.

– Capital continues to rotate out of the commodity currencies and into European FX.

– Ultimately, the EURUSD pulled back from $1.3800 as US yields rose before FOMC.

The Euro was once again a top performer this past week, gaining slightly overall against its major counterparts in what turned out to be volatile, yet constrained, trading conditions (finishing just behind the top performer, the Canadian Dollar, by -0.26%). No single currency gained or lost in excess of -0.56% against the Euro this past week except for the Australian Dollar (EURAUD +1.78%), as market participants used the lighter data week to position for key event risk on the horizon (indeed, the brief commentary that sent the Aussie tumbling was the highlight of the week).

A major reason for support for the Euro in recent weeks has been a lack of new easing measures from the European Central Bank. Although a FLS-like LTRO may be in the works, many have correctly pointed to the dramatic contraction in the ECB’s balance sheet over the past year as a reason for the Euro’s elevated exchange rate. The ECB’s balance sheet has declined by -24.6% in the 52-weeks ending December 6, 2013; to contrast, the Federal Reserve’s balance sheet has grown by +36.8% over this same period; and the Bank of Japan’s has growth by +40.7%.

Taking these data a step further, we see that the ratio of the Fed’s balance sheet to the ECB’s balance sheet – which stood at 0.96 this time in December 2012 – is now at 1.72. On a relative basis, the Fed’s balance sheet has grown +79.2% relative to the ECB’s over the past year. We believe this has been the prime reason for a generally improving EURUSD in 2013. As such, any data or event that could alter the dynamic behind the Fed’s and the ECB’s balance sheets is paramount.

Accordingly, our focus this week for the Euro is not solely on domestic developments but rather from those abroad (this will be a major theme across FX, not just the Euro). The Fed’s policy meeting on Wednesday should prove to be rather disruptive to markets, irrespective of what else might be happening fundamentally or technically, as it did in on June 19 (beginning of taper speculation) and September 18 (surprise non-taper decision).

The Euro’s role in the Fed’s taper production is complicated. In June, the Fed meeting marked a two month top in the EURUSD as the pair slid from above 1.3400 at the time to under 1.2800 over the next four weeks. Yet with the USDJPY rallying, the EURJPY, after seeing several multi-hundred point swings in the days after the June FOMC, eventually settled higher. The EURAUD took a straight line up. In the “taper on” environment, the Euro suffered against the US Dollar, was at first neutral against the low yielding safe havens, and appreciated sharply against the commodity currencies.

We highlight these outcomes as it is possible the market isn’t positioned for a QE3 taper in the slighted. True, US yields have risen over the past several days; but consensus estimates for the composition of QE3 show that $85B/month in asset purchases is still expected going into 2014. A non-taper outcome, like in September, could produce a swiftly weaker US Dollar, and strength developing in the higher yielding and emerging market currencies (at the Euro’s expense). But if the Fed does taper, market participants, by and large, will be caught off guard. Indeed, the disruptive nature of the FOMC decision this week could unhinge FX markets from recent trends,tempering any impact seen from any Euro-borne developments over the coming days. –CV

To receive reports from this analyst, sign up for Christopher’s distribution list.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx