US Dollar: Make or Break Week as the Fed Decides the Taper

Fundamental Forecast for US Dollar: Bullish

Dollar suffers significant bearish break on biggest S&P 500 rally this year

Fed mouthpiece Hilsenrath sets tone for critical June policy decision

US Dollar looks to set up strong trading opportunities for mid-week

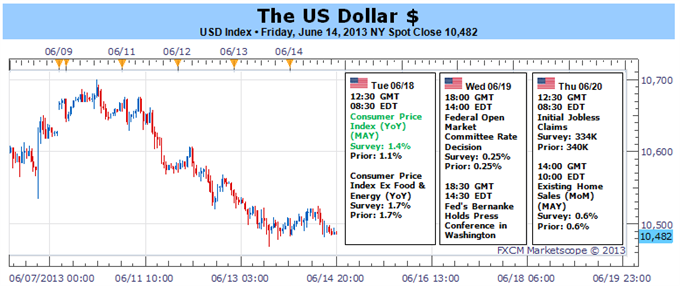

The Dow Jones FXCM Dollar (ticker = USDollar) endured a critical tumble this past week – a move that threatens to seismically alter a nine-month bull trend for the currency. Yet, both technical break and trend ambitions can be immediately reversed by one critical piece of event risk: the Federal Reserve’s June rate decision. Already an important event for gauging the level of external support for investor sentiment and US rates, the market-moving potential surrounding this affair has been amplified by heavy speculation, a poor reaction from Japanese markets to BoJ QE and the slow realization of excessive leverage in the market.

Monetary policy – particularly that of the Federal Open Market Committee (FOMC) – is a critical part of the market infrastructure at this point. Back in the rout of 2008, the first moves were made by the Fed and Treasury to prevent a collapse in the financial system – a noble cause. After the first quarter of 2009, though, the central bank moved back to its primary mandate of promoting steady inflation and full employment. The first quantitative easing (QE) programs were aimed at reducing market rates further than the cuts to the Fed Funds rates could achieve. In the more recent phase of the recovery, the objectives of policy have blurred. While the mandates remain, an obvious and dangerous side effect has resulted from the support: the capital market’s dependency on stimulus to charge record highs. We almost certainly wouldn’t have seen a record S&P 500 so soon if it weren’t for QE2 and QE3, so what happens when the programs end? Will innate growth and investment simply supplant the moral hazard and keep us at record highs? Unlikely.

The June 19th policy decision is not our run-of-the-mill Fed event for a number of reasons. First and foremost, this is one of the group’s quarterly events in which they deliberate policy, update forecasts (growth, inflation and interest rates) and offer up Chairman Bernanke for a press conference. As a monetary policy authority, this is an ideal opportunity to explain a difficult decision to a market that is almost certainly prone to ‘over-reacting’ (a term that central bankers and economists would use, but traders should recognize is inappropriate). A difficult period does lie ahead for the Fed: the ‘Taper’. This term refers point at which the $85 billion-per-month purchases of Treasuries and Mortgage-Backed Securities (MBS) under the QE3 program are finally reduced. This would not represent a tightening in policy, rather it is a reduction in the pace of expansion.

The difference between the Taper and an actual unwinding in stimulus or rate hike is severe. Yet, that won’t matter to the market. Speculators are forward looking. They front-run what is likely to happen in the foreseeable future. Just as industrious traders have moved in ahead of the Fed by buying Treasuries or applying leverage to markets like stocks, they will also look to pull back before the central bank does. That means that an announcement that the monthly stimulus clip will be reduced can very likely send the market in a scramble of risk aversion – a move that could cave over-extended capital benchmarks (S&P 500) and rally safe havens (like the dollar).

What is the chance that the Fed announces a tapering at this June meeting? It is less than 50-50. While we have seen an improvement in data since the last policy decision and tempering of the equities markets has been steady, there is benefit in spending more time acclimatizing the market to the reality that the support will eventually be reined in. Looking at the balance of biases amongst the FOMC voters, there are few calling for an immediate pullback. Key members that fall into the ‘neutral’ category have suggested they would prefer 2-3 more months of data. That would work with Bernanke’s Congressional testimony that a taper could occur within the same time frame.

For trading scenarios, an actual move to reduce QE purchases would be seen as a surprise to the bulk of the market; and the risk aversion impact would be severe. A smaller reduction (such as a modest $5 billion slowing) would generate less short-term volatility, but it would set off a wave of deleveraging through the medium-term regardless. A larger cutback ($10-25 billion) would combine both serious volatility and trend. That said, the more likely outcome is to keep the program as is for this month.

Should we come through the program with no change to the stimulus programs, we could still end up with a serious trend development via guidance. If Bernanke uses his press conference or statement to warn the market that the next regular or September meeting will introduce the inevitable shift, the front-runners will take it as a sign. There is little chance of an outcome that provides anything longer than a short-term bullish reaction for risky assets (bearish for the safe haven dollar). – JK

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx