Fundamental Forecast for Gold:Neutral

Gold and Silver Dip As US Dollar Gains Following FOMC Minutes

Gold Dip Underway; Former Range High at 1279 is Now Support

Sign up for DailyFX on Demand For Real-Time Gold Updates/Analysis Throughout the Week

Gold prices nudged higher this week with the precious metal advancing 0.25% to trade at $1322 ahead of the New York close on Friday. Equity markets also closed higher on the week with the Dow, S&P and NASDAQ posting more than 0.55% gains across the board. One would inherently look to weakness in the greenback to account for some of the gains in gold but a closer examination sees the Dow Jones FXCM USDOLLAR index closing the week higher by 0.55%. So what gives?

Since the 2013 low made on December 31st, gold prices have rallied more than 11% with weakness in the greenback and broader volatility in equity markets fueling demand into the perceived safety of the yellow metal. But the risk-off argument only goes so far. The relative strength and breathe of the advance now suggests that there may be a broader shift in the fundamental outlook for bullion as prices advanced this week alongside both the US dollar and equities. A notable increase in physical demand out of China and other EM markets have also continued to be supportive with investors stepping back in as prices rebounded off 6-month lows.

The largest fundamental threat to the rally would be a more aggressive taper stance from the Federal Reserve- a scenario that would likely fuel demand into the greenback as interest rates track higher and inflation expectations soften. That said, recent softness on the data front is unlikely to prompt such a stance with housing starts, building permits and existing home sales all coming in below consensus estimates this week. The news comes on the back of a string of weaker-than-expected prints on non-farm payrolls, ISM manufacturing, retail sales and industrial production this month and brings into question the health and sustainability of the recovery.

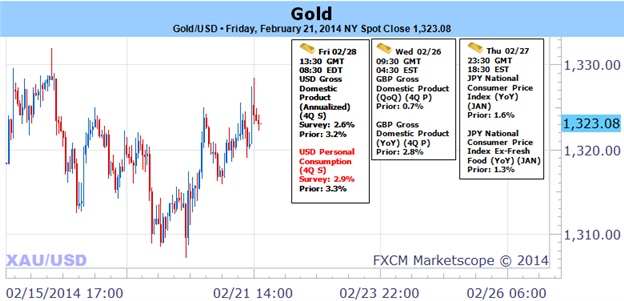

Heading into next week, traders will be eying more comprehensive housing data with the S&P / Case-Shiller home price index, new home sales and pending home sales on tap. Highlighting the economic docket will be the release of the revised 4Q GDP figures with consensus estimates calling for a downward revision to an annualized rate of 2.5% q/q from 3.2% q/q. Should the recent softness in US data persist, look for expectations of a delay in the Fed’s taper to begin taking root with such a scenario likely to be supportive of equities & gold / heavy for the dollar.

From a technical standpoint, the recently rally off the December low is now vulnerable and while we anticipate higher prices in gold, we will take a neutral stance below key resistance at $1336/38. This region is defined by the 100% extension of the advance off the 2013 low and the 61.8% retracement of the decline off the August high. Also note that a longer dated trendline resistance dating back to the 2012 high comes in just ahead of $1336 and if compromised suggests a much more significant low was put in place back in December. Such a scenario eyes topside targets at $1360, $1400 and $1415. Interim support rests at $1295/99 with our broader outlook remaining weighted to the topside while above $1268/70. –MB

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx