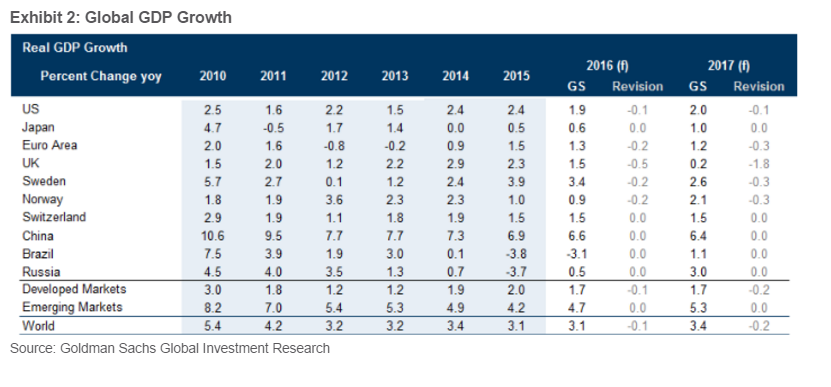

A: The most significant change is a sharp cut in our UK GDP forecast by a cumulative 2¾% over the next 18 months, which implies that the economy enters a mild recession by early 2017.

We have also reduced our Euro area GDP forecast by a cumulative ½%, which implies an average growth rate of 1¼% instead of 1½% for the next two years, and have shaved our US GDP forecast for the second half of 2016 by ¼pp to 2%.

There are three economic transmission mechanisms for the Brexit shock.

First, the UK terms of trade are likely to deteriorate, especially if it becomes harder to export high-value added services (including financial services) to the European Union. This is probably the most important shock from a long-run perspective, although its size is highly uncertain because we do not yet know how much access the UK will ultimately have to the Common Market.

Second, the uncertainty about the long term is likely to weigh on UK growth in the short term as firms hold off on investment. There is a substantial body of economic research showing that uncertainty shocks have large negative macroeconomic effects. Our European economics team views the uncertainty shock as the main near-term drag on UK growth.

Third, outside the UK the main transmission channels are weaker UK demand for imports and—much more importantly—a tightening of financial conditions via a stronger exchange rate and lower risk asset prices.

Taking as given the hit to UK GDP projected by our European economics team and the changes in financial conditions seen on Friday, we use the model to estimate the impact of the Brexit shock on growth in the major economies over the next two years. We then feed the GDP hit into an inflation hit via a Phillips curve relationship that also has a role for exchange rate pass-through.

And finally, we feed both the GDP hit and the inflation hit into a change in the warranted short-term interest rate via simple Taylor rule relationships.[3] The upshot is that the assumed hit to the UK and the moves seen in financial markets so far imply only moderate economic spillovers. The GDP effects are consistent with the forecast adjustments in the Euro area and the US already announced, although they suggest that Japan is at risk of even weaker growth than our Japan team’s ½-1% forecast for 2016-2017 if Friday’s FCI tightening does not reverse. The inflation effects are generally very small; only Japan sees a hit of more than 0.1pp because of the size of Friday’s trade-weighted yen appreciation. And finally, the monetary policy effects are moderate, with a reduction in the warranted policy rate relative to the baseline of between 20bp in the US and 50bp in Japan.

Copyright © 2016 Goldman Sachs, eFXnews™Original Article