Fundamental Forecast for Euro: Bullish

Euro Falls Below $1.3000 on a Suggestion of Further ECB Intervention

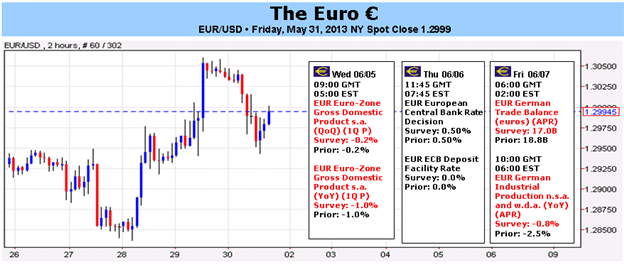

EUR/USD Fights for $1.3000 amid Month-End Rebalancing

EUR/USD Stays Buoyant Despite Dip Below $1.2900

The Euro was a top performer this week despite flashes of excessive volatility – the EURUSD saw prints close to $1.3100 and 1.2800 – as a slight uptick in data coupled with general anxiety over several of the single currency’s counterparts allowed gains to be found. To be clear: the Euro-zone economic picture is still horrid, with the region’s Unemployment Rate hitting 12.2% in April, an all-time high; while the youth Unemployment Rate (25 years old and under) continue to skyrocket, now at 62.5%. Certainly, there is a social crisis resulting from the economic crisis, an issue that will become more prevalent in the coming months as the US economy trends higher – on a relative basis, making Europe look that much worse.

Luckily for the Euro, issues outside of the region are garnering a great deal more attention at present time, affording it the opportunity to continue to post sizeable gains against the commodity currencies especially. Political tensions have been reduced to a low simmer in recent weeks, as the global economy seemingly waits around for the German elections in September because, let’s face it, there aren’t going to be any substantive shifts in the core’s stance on austerity until Angela Merkel can be sure that she retains her chancellorship.

On the austerity front, some good news emerged, offering support to the bullish Euro backdrop that has emerged since mid-May. Midweek, it was announced that the European Union had ended its excessive-deficit procedure against Italy. This is the first step in the right direction for the Euro-zone’s third largest economy, and perhaps it means that some fiscal stimulus may be on the horizon. Still, the European Commission warned that austerity should continue,in order to reduce the country’s fiscal deficit from the 5.5% of GDP in 2009 to the 3.0%threshold required under EU regulations – which was supposed to be accomplished by last year. Given the current trajectory of the deficit, the EC’s Italian forecast calls for a further reduction to 2.9% in 2013 and 2.5% in 2014.

Ultimately, these two data points offer an interesting juxtaposition for policymakers: on one hand, the region’s labor crisis has never been worse; on the other, one of the biggest perpetrators of excessive debt accumulation has made significant progress. The policies are seeing their intended purposes, but at a harrowing cost.

The first chance to see where the European Central Bank stands on the issue will come this week, as pressure has shifted back to the central bank to do something, anything, to help revive lending in the region. As per data released on Wednesday by the ECB, loans to the Euro-zone’s fell by -0.9% y/y in April, worse than the -0.7% y/y forecast. This was the twelfth consecutive month of contraction, underscoring the hesitancy of banks to inject capital into the periphery. The core faces no such issue. There is an obvious and prevalent dichotomy between credit growth in Germany versus Spain, for example: loans in Germany were up by +0.3% y/y while they contracted by -8.8% y/y over the same reporting period.

Thus, as the ECB grapples with what to do next to spur lending, there’s likely to be significant discussion over the efficacy of a small- and medium-sized enterprise (SME) lending program, aimed at provoking banks to pass on the easy credit conditions the ECB has provided. One such measure being discussed is the implementation of negative deposit rates. Deposit rates are what the ECB pays to banks for keeping their cash held at the ECB; negative rates would force the banks to pay the ECB – destroying capital. This should incentivize banks to step up loan originations, but also boost capital spending – both of which would provide a much needed boost to the economically and social depressed region.

While negative deposit rates would certainly be negative for the Euro, at this point in time, it is unlikely that the ECB takes the plunge – for now. Division remains, despite Italian ECB Governing Council member Ignazio Visco sayingon Friday that the ECB “stands ready to intervene” to push yields lower. Three prominent ECB officials – Vice President Vitor Constancio, Joerg Asmussen, and Christian Noyer – indicated that negative rates are still in the initial stages of discussion, and that the ECB is not near implementing them. Accordingly, with the ECB Rate Decision on Thursday as the most prominent Euro-zone event on the calendar this week, a policy hold could relieve some of the priced-in negative rate pressure on the Euro, affording it the opportunity to rally into the end of the first week of June. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx