Euro Outlook Muddled by Italian Politics, Weak PMI Data

Fundamental Forecast for Euro: Neutral

Aussie and Kiwi Rebound Alongisde Gold; EUR/USD Above $1.3100

Euro Remains Capped Despite ECB Hopes

EUR/USD Nasty False Break – Support 1.2970

The Euro had a surprisingly strong week, losing ground only to the US Dollar by -0.47%, with the EURUSD settling at 1.3054 at Friday’s close. The European currencies on the whole regained favor this past week after Chinese 1Q’13 GDP severely damaged the commodity bloc’s prospects for gains. The Euro climbed by +1.74% against the Australian Dollar and +1.52% against the New Zealand Dollar, although further gains are in question. This past week we saw the Italian parliament remain split over who to elect to the Italian presidency, and now Center-Left leader Pier Luigi Bersani has announced that he will step down from leadership.

The main piece of commentary on the week that helped keep the Euro elevated came from German Bundesbank President Jens Weidmann, who said that [we] “don’t expect too much” from a rate cut, signaling that hawkish monetary policy would continue to be a counterweight to any further efforts to accommodate policy further. This is not ‘news’ per say: we have heard many times that the European Central Bank’s policy transmission mechanism is broken, or that monrey simply isn’t being created in the economy thanks to deleveraging. Mainly, this symptom is affecting Italy and Spain, but it’s clear that it will be hurting France and Germany in the future if growth prospects don’t improve soon.

Inherently, this is hawkish commentary, because it means that ECB policymakers aren’t likely to cut its key rates at the next meeting in May, removing a weight on yields in the region, and keeping the Euro higher. But when in considered in sum with the Italian political meltdown – a policy bottleneck – and the data due this coming week, we must hold a neutral outlook for the single currency.

In terms of market moving data due this week, while there are no “high” significant events according to the DailyFX Economic Calendar, there are several “medium” impact events that will drive price action. By all estimates, there will not be a material shift higher in growth expectations for the major European economies, keeping the recession on trajectory to remain in place well into the 2H’13 (as opposed to ECB President Mario Draghi’s insistence that growth would recover “later in the year).

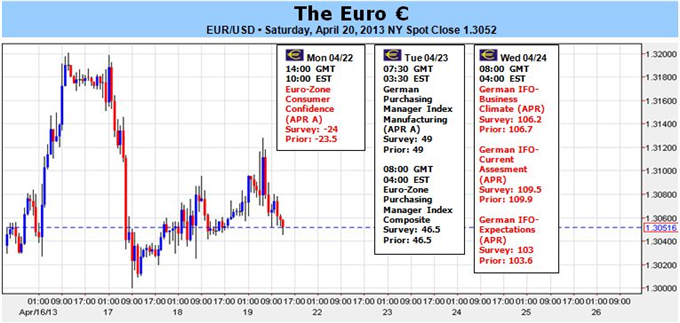

On Monday, the Euro-zone Consumer Confidence (APR A) index will fa ll to -24.0 from -23.5, as the impact of the Cypriot bailout is begun to be felt in European data. On Tuesday, the cascade of European Purchasing Managers Index data will be the highlight of the week, but weakness throughout – a smaller degree worse off, but still in contraction territory. The German PMI Manufacturing (APR A) report will remain on hold at 49.0, while the German PMI Services (APR A) report will tick higher to 51.0 from 50.9. In the broader Euro-zone, PMI Manufacturing (APR A) index will dip to 46.7 from 46.8. The PMI Services (APR A) report will increase to 46.5 fr om 46.5.

In the context of this data, we see that the region’s worst economic climate since the depths of the global financial crisis will remain in place, and as long as the ECB doesn’t believe that any further reasing in monetary policy will do much good – at least according to Bundesbank President Weidmann – we must taken a neutral bias for the Euro. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx