Euro Hurt by Shift in ECB Policy, Bearish Fundamental Pressures Turned Up

Fundamental Forecast for Euro: Bearish

ECB’s New Policy Tool Slams Euro

EUR and GBP and Fresh July Lows

Momentum Scorecard: Euro is Weak, but British Pound is Weaker

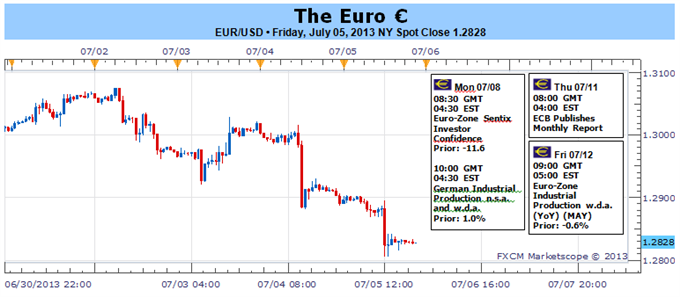

The Euro finished the week mixed overall, sliding another -1.41% against the US Dollar (with the EURUSD closing down at $1.2829), while posting gains against the British Pound (+0.74%) and the Japanese Yen (+0.65%). Indeed, the Euro’s performance was dramatically altered by the end of the week thanks to the new policy tool of the European Central Bank – “forward guidance” – which should help keep rates low, and accordingly the Euro weaker, over the next several years. ECB President Mario Draghi’s pivot towards a more dovish policy stance came as a bit of a surprise, considering that recently ECB policymakers have been suggesting that a shift to negative deposit rates remained a distant possibility in the near-term.

So, with the ECB taking a page from the Fed’s playbook (the Bank of England is, too), there’s a clear signal that policymakers will work to keep short-term interest rate tethered near zero. While Italian and Spanish bond yields have come down modestly in the wake of the ECB’s announcement on Thursday, the big picture is that peripheral yields are up sharply from early-May, before the Fed’s “taper” talk heated up.

Clearly the ECB’s shift is in response to tighter conditions from the Fed; and as the Fed tightens, the ECB will be forced to ease further to keep rates pinned lower – or at least using forward guidance in a more extended capacity – which should put pressure on rates in favor of a weaker EURUSD. Already this week the US-German 10-year note yield spread hit its widest level since October 2006, a sign of the burgeoning US Dollar strength.

As this new theme surrounding the ECB’s new policy tool develops, the other non-economic data influence on the market recently has been calmed – the mini-Portuguese political crisis has been stemmed. Junior coalition members were threatening to pull support (the main opposition party is leading in the polls), but the difference between the Portuguese government upheaval versus the Greek one last spring is that the main opposition party isn’t fervently anti-austerity/anti-Euro

Even in the event of new elections down the road, it is unlikely that there is any major shift from the current austerity program considering the main opposition party signed the IMF’s “Letter of Intent,” meaning that any negative influence Portuguese politics has on the Euro is transitory at best.

Taking a look at the docket, the calendar is significantly lighter this week although German data is in focus. In particular, the final June German CPI reading is due, which should show that price pressures remain below the ECB’s +2% yearly target. At this point in time, the data will do little to shake stronger fundamental headwinds, despite the possible hawkish implication; but these are not normal times, and with the rest of the Euro-Zone facing a deep recession, any upside the Euro sees may be short-lived going forward.

— Written by Christopher Vecchio, Currency Analyst

To contact Christopher Vecchio, e-mail cvecchio@dailyfx.com

Follow him on Twitter at @CVecchioFX

To be added to Christopher’s e-mail distribution list, please fill out this form

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx