Fundamental Forecast for Euro: Neutral

– EURGBP falls to and holds key support despite weak Euro-Zone data, ECB rate cut.

– Better than expected US data (3Q’13 GDP, October NFPs) at the end of the week kept the EURUSD pinned down.

– For real-time news, data, and technical analysis on the Euro, sign up for DailyFX on Demand

The Euro’s bullish momentum seen gathering since July – both fundamentally and technically – evaporated this week after the European Central Bank surprised market participants with a 25-bps rate cut. With the ECB’s main refinancing rate now at a new record low – and the same level of the Federal Reserve’s main rate – any carry advantage the Euro might have held against the safe haven currencies has diminished, tainting the appeal of the single currency.

The timing of the ECB rate cut comes at a curious time, with market participants widely expecting no change in policy (credit markets implied only a 4.1% chance of a 25-bps rate cut ahead of the meeting). Peripheral growth has remained weak in recent months, though off the lows; so to say that this policy decision was aimed at helping Italy or Spain, for example, is a bit far-fetched. A look at recent German data, though – month-over-month CPI came in at -0.2% for October – shows that the ECB rate cut is more or less a reaction to evidence of a slowing German economy.

Ironically, the Euro’s weakness the past two weeks may help alleviate the disinflationary and deflationary pressures starting to hit the region: a weaker currency will push up the cost of imported goods. Furthermore, a weaker currency will make peripheral exports appear cheaper to foreigners, as exchange rate differentials shift purchasing power abroad. Several months of a weaker Euro would do well to help the region pad its economic cushioning (even if the gains are superficial as a result of the ongoing currency devaluation wars).

Concurrently, the impact of the US Dollar on the Euro this week can’t be dismissed. Both the 3Q’13 GDP and October NFP reports exorcised US government shutdown demons, stoking a sharp uptick in US Treasury yields by the close Friday. With the “belly” of the US yield curve steepening the fastest, it appears that markets are starting to lean towards expecting a QE3 taper in December. As a result of these events and the ECB meeting, widening interest rate differentials – heading lower in the Euro-Zone and higher in the US – should favor further downside pressure in the EURUSD over the coming weeks.

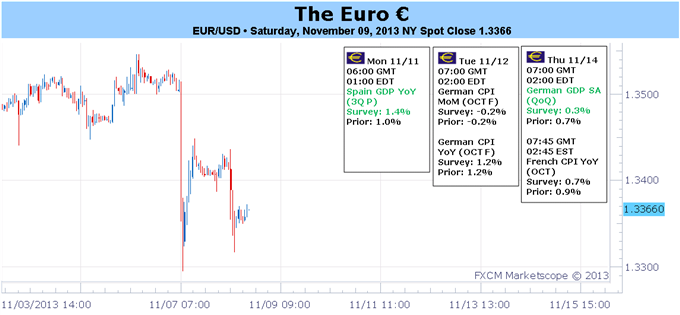

Going forward, we have data out of the Euro-Zone this week that will immediately impact market psychology in the wake of the ECB. With deflation concerns afoot, the various 3Q’13 GDP readings due out this week (among others) will confirm or repeal those issues, offering opportunity for both EUR-positive and –negative outcomes.

On Tuesday, the final October German CPI report will be issued, and confirmation that the monthly gauge remained in deflation territory (-0.2% expected unch) will keep the door open for further accommodative policies in the future: this past week’s policy decision made clear the ECB’s intent to shape policy solely around Germany (otherwise the main rate would have been cut months earlier). Without German monetary indicators pointing towards deflation, other easing policies – another rate cut, another LTRO – are highly unlikely. It is important for Euro bears that German data, more so than any other country, continues to remain under pressure.

The slowdown in regional inflation has raised concerns so quickly because of the implications to growth: weak inflation in developed countries historically coincides with slowed demand. On Wednesday, a trifecta of growth readings will crystalize these views. French, German, and broader Euro-Zone 3Q’13 GDP readings are all expected to be meager at best.

The negativity might be priced in – after all, the ECB cut its main rate. The risk to the Euro, then, could be to the upside: beats will generate more enthusiasm than misses will. (Very similar to the sentiment surrounding the US Dollar ahead of the October NFP report, though not as intense.) Accordingly, while our medium- and longer-term views are becoming more bearish on the Euro, we must be aware of short-term risks to the upside. –CV

To receive reports from this analyst, sign up for Christopher’s distribution list.

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx