Fundamental Forecast for Euro: Neutral

Euro to Rally as ECB Fails toImplement Negative Rates

EUR/USD Overtakes $1.3100, EUR/JPY ¥130.00 amid ECB Press Conference

US Dollar Starts June Lower, EUR/USD Set to Hold $1.3000 This Week

The Euro finished squarely in the middle of the currencies covered by DailyFX Research this week, dropping -1.26% against the reinvigorated Japanese Yen (having recovered from losses from as great as -3.41%), while gaining +1.66% against the US Dollar (having given back gains from as great as +2.36%). Mainly, the Euro’s gains were following through from the prior week, when the EURUSD broke out of a bullish technical congestion pattern.

Building on the near-term bullish technical structure in place, the EURUSD found gains in the second half of the week after the European Central Bank held the line on its monetary policies and failed to implement negative interest rates (as we suspected). Overall, the tone at ECB President Mario Draghi’s meeting suggested that the recent uptick in May data was enough to put the implementation of negative deposit rates on the sidelines for at least the next several weeks (but not necessarily off the table entirely). Although sovereign spreads between peripheral and German yields burst wider – an indicator of increased Euro-zone financial stress – the Euro managed to climb to its highest level since February 25 against the US Dollar, hitting $1.3306 on Thursday.

While the Euro gained against the US Dollar, it’s important to note that its performance elsewhere was mediocre at best overall, as the massive unwind of US Dollar longs provoked a general diversification into the other safe havens, the Japanese Yen and the Swiss Franc. Sincerely, it’s not a strong sign that the Euro only outperformed the commodity currencies elsewhere – that hasn’t been considered a feat of accomplishment in the 2Q’13. It seems that the market isn’t convinced by the ECB chief’s not-so-dovish view.

True, he may be overly optimistic: the region’s Unemployment Rate is at an all-time at 12.2%; and the youth labor situation (24 and under) in the Greek and Spanish labor markets have Unemployment Rates greater than 55%. Inflation is nonexistent because consumers don’t have substantial enough disposable income to drive prices higher – an indication of increased aggregate demand. As noted last week, as per data released last Wednesday by the ECB, loans to the Euro-zone’s fell by -0.9% y/y in April, worse than the -0.7% y/y forecast. This was the twelfth consecutive month of contraction, underscoring the hesitancy of banks to inject capital into the periphery. The core faces no such issue. There is an obvious and prevalent dichotomy between credit growth in Germany versus Spain, for example: loans in Germany were up by +0.3% y/y while they contracted by -8.8% y/y over the same reporting period.

These factors add up to a meager growth situation in the Euro-zone, which saw the final 1Q’13 growth figure drop to -1.1% y/y from -1.0% y/y, while the quarterly rate remained at -0.2%. Data this upcoming week will remain on the soft side, beginning with the final 1Q’13 Italian GDP report on Monday. Considering the revision lower in broader regional growth rate, it’s possible that Italy was the perpetrator. A reading of -2.3% y/y is expected.

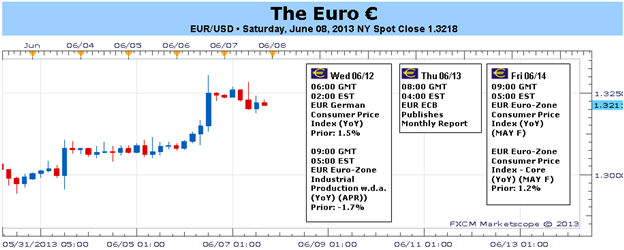

On Wednesday, the first bit of inflation data for the week is due, when the final May German Consumer Price Index figures are released. On the headline, +1.5% y/y is expected; on the core, +1.7% y/y is expected. Both of these figures undershoot the ECB’s +2% yearly inflation target, adding some credibility to the belief that Germany will become incrementally more open to accommodative monetary policy. Similarly, on Friday, the final May Euro-zone Consumer Price Index figures will be released, and these too will undershoot the ECB’s target medium-term target, but more severely: the headline is expected at +1.4% y/y; and the core is expected at +1.2% y/y.

While recent data has been slightly brighter, the negative implications of the major data due this week outweigh the other ‘medium’ ranked data interspersed, such as the June Euro-zone Sentix Investor Confidence report on Monday (-11.3 expected from -15.6) and the May Euro-zone Industrial Production report on Wednesday (-1.1% expected from -1.7% (y/y)). At this point in time, we think a more neutral outlook for the Euro is applicable, especially considered in context of recent volatility in the CHF-, JPY-, and USD-based pairs. -CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx