As expected no changes in rates came forth from the ECB yesterday, in his conference call ECB president Mario Draghi upped the growth forecast for 2016 from 1.4% to 1.6%, and even inflation is expected to pick up later this year improving to 0.2%.

ECB is expecting economic growth to continue at a moderate but steady pace, but Mr Draghi also warned of the global downside risks and specifically the Brexit vote on the 23rd of this month.

Early into today’s session we saw that growth in the services sector for the world’s second largest economy eased when compared to the previous reading down 51.2 from the previous 51.8.

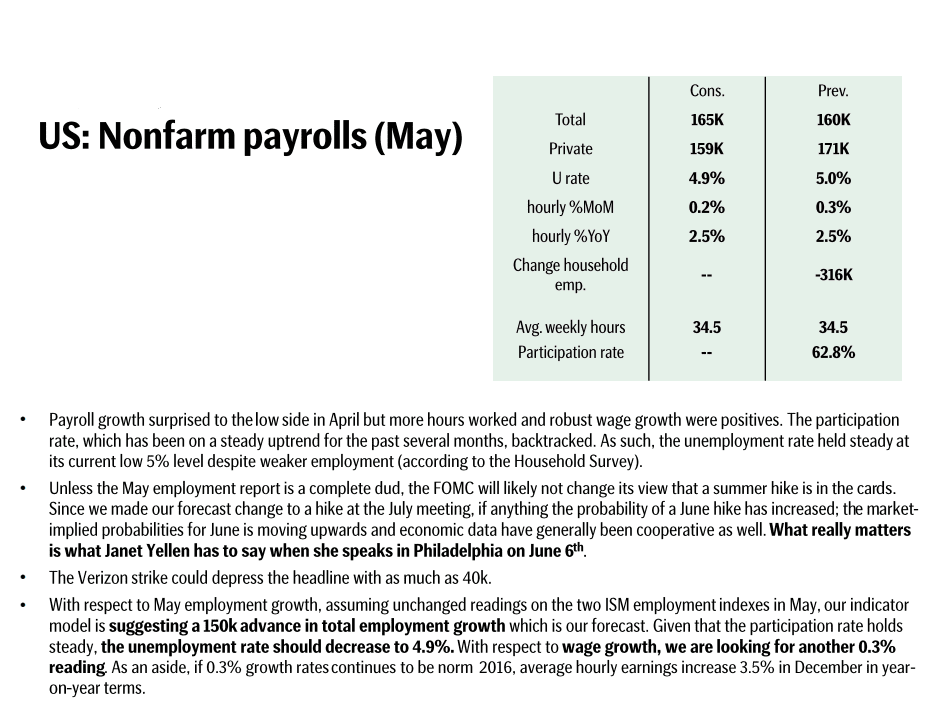

Again from the economic docket today, the highlight shall go to the health of the US labour market as speculation runs rampant about a june rate hike and the Fed continues to iterate that hikes are still very much in the cards.

The greenback has done well for itself rising over 4% from 03rd May lows a month ago. On the other hand the hand the GBP is lower across the board and has had to struggle lately ahead of the Brexit vote later this month.

Today the USD takes the limelight as traders eagerly await US Nonfarm payrolls and unemployment rate – unemployment is expected to eased further to 4.9%.