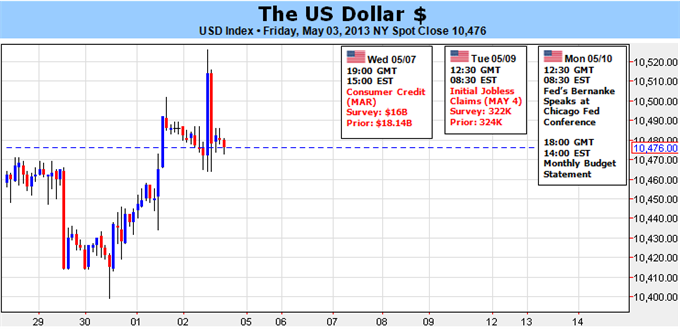

Dollar in Danger of Major Trend Shift Despite Thin Docket

Fundamental Forecast for US Dollar: Neutral

Dollar retreats from critical, bearish breakdown after Fed remains mum

NFPs increase more than expected, unemployment rate drops

USDollar in the middle of its range as the S&P 500 hits a record high

The dollar experienced a tumultuous period on the fundamental front this past week – an unflattering one if we consider its role as the world’s favored safe haven currency. Yet, despite the negative implications through traditional channels, the Dow Jones FXCM Dollar Index (ticker = USDollar) managed to hold its two-month congestion pattern just off a two-and-a-half year high. The benchmark currency seems anchored and unyielding to questionable events that contradict underlying themes. However, the market won’t be able to avoid commitment for much longer – especially with central bank-supported risk taking driving the S&P 500 to record highs.

As has been the case for months, the dollar’s primary interests remain ‘risk appetite’ and stimulus expectations. And, those two stories are certainly interwoven. Yet, if these two concentrations are so influential, why did the heady mix from this past week not send EURUSD rallying above 1.3250 and AUDUSD to seek out 1.0600? The Federal Open Market Committee (FOMC) policy decision was an event whose outcome was very much in the eye of the beholder. The policy group noted improvement in the labor force while hedging themselves with a warning of ‘downside risks’ to the economy. The real interest, though, was what level of guidance they would offer for the extra-ordinary quantitative easing program. An efficient market has worked to price in the $85 billion-per-month QE3 purchases likely through the end of the year, so any definitive sign of tapering could prove problematic.

Perhaps officials recognized the risk to the capital markets if they moved too early in warning of a shift in their exceptional stimulus scheme, because the statement was nearly as untouched as the policy itself. However, there was one meaningful alternation. The Fed made the express move to suggest it was prepared to “increase or reduce” its QE purchases in the future as warranted. This may seem insignificant; but seen from a central bank’s perspective, it is a critical first step. In a perfect reflection of Game Theory, the central bank has to make measured moves with the express knowledge that the market will react to each step with responses that change the environment. Stimulus from the Fed and its peers have unquestioningly influenced the market by driving benchmark yields (and there all rates of return) to record lows while the assumption of risk has evaporated. This has led to a tangible chase for yield where none is to found. Capital gains are the only way to sustain this move, but gravity remains as new heights are scaled.

By telling the market that they are ready to make small changes, there should be relatively little surprise should the next Fed meeting – which fittingly enough will include updated growth, inflation and rate forecasts along with Chairman Bernanke’s press conference – report a test move to decrease the monthly purchases. Of course, even if this were the plan, it may not change the outlook for the risk trends and the dollar unless the masses were privy to it. Therefore, every opportunity to weigh the balance of sentiment amongst the Fed officials is a means for tipping the scales. Looking at the docket ahead, there are a number of officials scheduled to speak (Bernanke, Lacker, Evans, George, PLosser, Stein, Pianalto) and the G7 meeting will no doubt bring international pressure for the Fed’s easy money.

If there is any tangible threat that the Fed will throttle back on its stimulus support, the impact on risk trends would no doubt be spectacular. Given the divergence between market pricing (S&P 500 at record highs) and fundamentals (yields at record low as growth slows), there is a tremendous discrepancy. And, the dollar would be well-positioned to take advantage. Not only would the smaller projected increase in the US money supply boost the dollar’s perceived value, but the exodus of capital from risk to safety would light a new fire under the currency. That said, not all dollar pairs would benefit such a move. Particularly USDJPY would find the dollar mimicking a carry/investment currency as the unwind in other yen-based crosses would overwhelm any positive influence here.

In terms of scale, disrupting the moral hazard that has allowed the incredible divergence between positioning and risk-reward balance is the greatest threat. The power of speculation is strong, so it isn’t difficult to feed fear that this will eventually happen, but that isn’t something we can mark on a calendar. In the meantime, dollar traders will have little event risk to work with this coming week and should instead keep an eye on the headlines and any sign that investors are simply trying to take profit in traditional assets. – JK

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx