Dollar Can’t Hold Gains, but Don’t Call the Rally Over Yet

Fundamental Forecast for US Dollar: Bullish

US Dollar tumbles on Nonfarm Payrolls disappointment

Federal Reserve meeting gives no details on “taper”, US Dollar pulls back

These are the key levels we’re watching on the USDOLLAR post-NFP’s

The US Dollar looked to take out key highs versus the Japanese Yen, Euro, and other counterparts. Yet a disappointing US Nonfarm Payrolls reportleft Dollar bulls wanting and yet the S&P 500 finished at record-highs – what might we see in the week ahead?

It was supposed to be a massive week for the Greenback with a Fed interest rate decision, Q2 GDP Growth data, and US Nonfarm Payrolls results for July. But the Dow Jones FXCM Dollar Index (ticker: USDOLLAR) saw four consecutive daily rallies yet never saw the substantial break higher we’d been predicting. If the top three economic events on the calendar couldn’t force a Dollar breakout, what could possibly do it?

The week ahead promises relatively little in the way of US economic event risk, and indeed volatility prices have tumbled in anticipation of fairly uneventful price action. Yet if there’s one thing that’s clear it’s that the next big market-moving event isn’t necessarily scripted.

The fact that the US S&P 500 trades at record-highs while Treasury Bonds and broader fixed income markets remain extremely volatile is clear reason for concern. And though it’s been a fool’s errand to try and time the top in the S&P, it’s worth noting that the Volatility Index (VIX) trades near its lowest levels since the onset of the financial crisis in 2007. Sentiment extremes are only clear in hindsight, but such clear levels of trader complacency leave plenty of scope for near-term corrections.

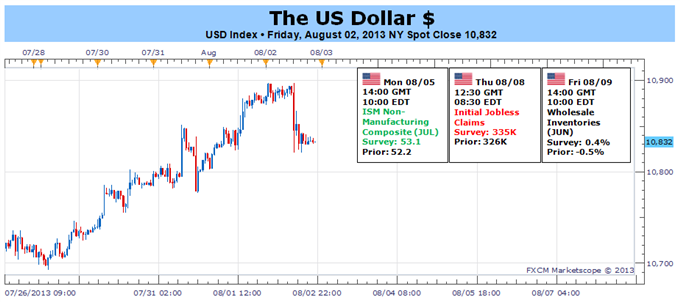

US economic event risk will be limited to ISM Services data due Monday and weekly Initial Jobless Claims on Thursday, and neither seem likely to force big moves given relative market indifference to US Nonfarm Payrolls data the US FOMC rate announcement. Instead we’ll look to the Asia-Pacific region for the top FX market events of the week.

A Reserve Bank of Australia interest rate announcement and Chinese trade and inflation figures could be the top market-movers for the Dollar Index—particularly as the Aussie and New Zealand Dollars were the worst-performing major world currencies through last week’s trading.

Fixed income traders are pricing in a 90+ percent chance that the RBA will cut interest rates at the coming week’s meeting. And though lower yields for the Aussie Dollar might not have a direct impact on the US economy, the fact that the Australian central bank remains in an easing cycle is significant for forex markets more generally. Expect noteworthy USD volatility on any surprises.

Chinese trade and inflation data could have important implications for closely-linked Australian, Japanese, and New Zealand economies to name a few. Clear dependence on Chinese consumption leaves the Aussie and Kiwi economies particularly susceptible if Imports disappoint. All the while, any above-forecast CPI/PPI inflation results could limit the People’s Bank of China’s options in keeping monetary policy loose in the world’s second-largest economy. Expect fireworks in the AUD, NZD, and even the JPY on any above or below-forecast prints.

Last week we claimed that the US Dollar was a potentially significant turning point versus the Yen and other counterparts. And though the Dollar Index failed to hold all of its gains, it’s worth noting that the USDOLLAR remains near key multi-week peaks after registering four-consecutive daily advances.

Was this the USD surge we were waiting for? Not exactly, but the month of August has thus far been kind to the Dollar Index. The week ahead could produce a continuation of Greenback gains. – DR

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx