Fundamental Forecast for the British Pound: Neutral

Speculative Sentiment Index Points to British Pound Weakness

GBP/USD Technical Analysis: Sellers Target Below 1.52 Figure

The British Pound was a bottom performer among the majors this past week, shedding -1.4% against the surging US Dollar, with the GBPUSD closing down at $1.5208 from 1.5417 to start the week. Although the Sterling didn’t post declines against the Japanese Yen – true risk aversion would have dropped the GBPJPY – weakness was quite prevalent as the GBPAUD, one of the top performers throughout the 2Q’13, fell by -0.5% to close at A$1.6641.

This past week, a surprise miss on the final 1Q’13 UK GDP report (+0.3% q/q unch, +0.3% y/y from prior +0.6% y/y) dramatically altered perception around the British Pound, and is likely to continue to be a negative influence in the coming weeks. The GBPUSD bottom in mid-March coincided with a turn in key data, with the PMI surveys showing broad improvement leading to hope that the economy accelerated, which would prevent the Bank of England from implementing any further accommodative policy measures that might weaken the British Pound. However, this ‘good feeling’ has dissipated, and it couldn’t come at a more critical juncture for the world’s oldest currency.

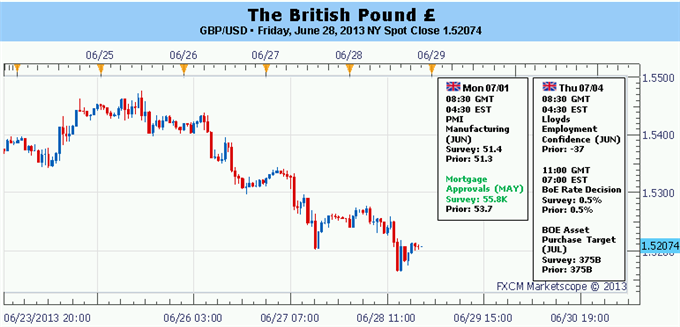

The BoE policy meeting on Thursday will be the first in the post-Mervyn King era, with former Bank of Canada Governor Mark Carney taking the reins. It has been long believed that Governor Carney’s ascension would be a consistent bearish influence on the Sterling, given the fact that from December 2012 through February 2013, on several occasions he suggested that central bank policy hadn’t reached its limit and that additional accommodative policies might warrant a consideration. In particular, Governor Carney has previously indicated that he might support a monetary policy that targeted a specific nominal GDP rate; this would entail, theoretically, the BoE easing at a faster pace (even in an ‘unlimited’ fashion like the Federal Reserve’s QE3), which would prove to be Sterling negative. Since the global financial crisis in 2008, the British Pound has depreciated by around -25% against its most highly traded counterparts.

With that said, despite the 1Q’13 UK GDP figure missing, Governor Carney is unlikely to implement any material or noteworthy policies at his first meeting this Thursday. As expectations for Governor Carney’s stewardship of the BoE are overall dovish, it is possible that a hold might lead to a brief burst higher for the GBP-based pairs.

Accordingly, renewed focus will fall on the PMI surveys due for June activity; they were instrumental in bolstering the fundamental base that helped boost the Sterling in late-May/early-June. Of note, June UK PMI Manufacturing should be unchanged at 51.3, PMI Construction should tick up to 51.3 from 50.8, and PMI services should steady from 54.9 to 54.6.

These figures highlight a modest growth picture for the UK, which at this point might not be enough to reproduce previous bullish sentiment surrounding the British Pound. Accordingly, we retain a neutral outlook this week, as any outperformance is likely to be short-lived, as a slowly recovering economy will prompt dovish policy actions from new BoE Governor Carney soon enough. –CV

DailyFX provides forex news and technical analysis on the trends that influence the global currency markets.Learn forex trading with a free practice account and trading charts from FXCM.

Source: Daily fx